13 Tax Breaks You Can Still Claim in 2026 Without Itemizing

Most Americans dread tax season. The paperwork alone feels like a punishment. Yet somewhere in all that stress, a surprisingly large number of people leave real money on the table, not because they did anything wrong, but simply because they didn’t know what they were entitled to.

Here’s the thing about the U.S. tax code: it’s built around itemizing, and most people assume that if they aren’t itemizing, they’re stuck with just the standard deduction. That’s not the full picture. There are powerful “above-the-line” deductions that reduce your adjusted gross income before you even make the standard versus itemizing decision. Some are brand new for 2026. Some have been quietly available for years. Let’s dive in.

1. The Standard Deduction Itself – Now Bigger Than Ever

Before we get to the above-the-line gems, let’s start with the foundation. For tax year 2026, the standard deduction increases to $32,200 for married couples filing jointly. For single taxpayers and married individuals filing separately, the standard deduction rises to $16,100, and for heads of households, the standard deduction will be $24,150. That’s not a small number.

The standard deduction increased by $350 for single filers and by $700 for joint filers compared to the 2025 tax year. Think of the standard deduction as your automatic tax shield. You get it no matter what, no receipts required, no justification needed. It’s the simplest tax break in the code, and for the vast majority of households, it is still the smarter choice.

2. Traditional IRA Contributions

If you set aside money for retirement in a Traditional IRA, you may be eligible for this common above-the-line deduction. This is one of those rare deductions where you do something smart for your future self and get a tax break right now. Honestly, it’s one of the cleanest deals in the tax code.

The maximum deduction for 2025 tax year contributions to a traditional IRA was $7,500 for most people, but it’s $8,600 for people who are at least 50 years old. You don’t need to itemize to claim it. With a Traditional IRA, you can still get a tax deduction without requiring access to an employer plan. However, your tax break may be limited if you also participate in an employer plan. Run the numbers, because it could be worth more than you think.

3. Health Savings Account (HSA) Contributions

A significant above-the-line deduction is for contributions to a Health Savings Account. An HSA is a tax-exempt savings account designed to help individuals save money for medical expenses. The contributions made by you or your employers are tax-free. Additionally, those distributions are tax-free when you access funds from an HSA account for qualified medical expenses.

For 2026, the HSA contribution limits are $4,400 for people who have individual coverage under an HDHP, and $8,750 for those who have family coverage under an HDHP. HSA contributions are deducted “above the line” on Form 1040, which means the deduction is available to filers regardless of whether they itemize deductions. Some people treat their HSA almost like a bonus retirement account, and with good reason.

4. Student Loan Interest Deduction

The student loan interest deduction allows eligible taxpayers to reduce their taxable income by up to $2,500 based on interest paid on qualified student loans. This deduction applies to loans taken out for higher education expenses, including tuition, fees and necessary supplies. Unlike some deductions, it is an above-the-line deduction, meaning taxpayers can claim it without itemizing.

The upper limits are a Modified Adjusted Gross Income of $100,000 for a single tax filer and $200,000 for a joint return. However, the tax benefits begin to be phased out starting at a MAGI of $85,000 for single and $170,000 for joint filers. Both federal and private student loans are eligible for the deduction. If you’ve been grinding through repayments, at least this small reward is waiting for you at tax time.

5. Self-Employed Health Insurance Deduction

For the self-employed, health insurance premiums became 100% deductible in 2003. The deduction allows self-employed people to reduce their adjusted gross income by the amount they pay in health insurance premiums during a given year. This is enormously valuable. Health insurance is wildly expensive, especially when you’re paying for it out of pocket as a solo operator or freelancer.

You may be able to deduct the amount you paid for health insurance, which includes medical, dental, and vision insurance and qualified long-term care insurance for yourself, your spouse, and your dependents. You can’t take the deduction for any month you were eligible to participate in any employer-subsidized health plan at any time during that month, even if you didn’t actually participate. A subtle but important rule – keep that in mind if your situation changed mid-year.

6. Self-Employment Tax Deduction

You can deduct one-half of your self-employment tax above the line. This one surprises people. When you’re self-employed, you pay both the employee and the employer share of Social Security and Medicare taxes, which is a painful double hit.

The IRS recognizes this unfairness, so they allow you to deduct half of that total self-employment tax directly from your gross income, regardless of whether you itemize. It doesn’t erase the burden completely. But think of it like getting a partial refund on money you had no choice but to pay. With working side hustles becoming more popular recently, it’s no surprise that self-employment expenses are more common.

7. Self-Employed Retirement Plan Contributions

Self-employed individuals can deduct contributions made to retirement plans such as SEP IRAs, SIMPLE IRAs, and qualified plans like 401(k)s. These contributions reduce taxable income and help self-employed taxpayers save for retirement with potential tax-deferred growth. For freelancers and business owners, this is one of the most powerful levers available.

For Simplified Employee Pension (SEP) IRAs, the maximum deductible amount for 2025 contributions is $70,000 or 25% of your first $350,000 of compensation. For self-employed taxpayers, SEP IRA and SIMPLE IRA contributions are “above the line” tax deductions. Put simply, the more you save, the less you owe. It’s one of those rare win-win situations the tax code actually hands you on a silver platter.

8. Educator Expense Deduction

Teachers spend their own money on classroom supplies constantly. It’s one of those widely known but rarely compensated realities of the profession. If you’re an eligible educator, you can deduct up to $300 (or $600 if married filing jointly and both spouses are eligible educators, but not more than $300 each) of unreimbursed trade or business expenses. Qualified expenses include participation in professional development courses, books, supplies, computer equipment, and supplementary classroom materials.

Starting in tax year 2026, educators can also deduct qualifying educator expenses as an itemized deduction without limitation. So the door has opened even wider for teachers going forward. The $300 above-the-line amount is small, no question, but it’s available without itemizing, and it’s one deduction that genuinely feels like the system giving something back to people who do a lot with very little.

9. The New Charitable Deduction for Non-Itemizers

This is a genuinely exciting development for everyday givers. The charitable deduction is normally an itemized deduction, but only about 10% of taxpayers itemize, with 90% using the standard deduction. Beginning in 2026, people who take the standard deduction and do not itemize will be able to get an income tax deduction for some of their charitable gifts. The maximum is $1,000 on single returns and $2,000 on married filing joint returns.

Only cash gifts qualify. You cannot get the deduction for gifts of household items or clothing. There are also a few charities that don’t qualify, including donor-advised funds, private grant-making foundations, and Section 509(a)(3) supporting organizations. Reducing AGI can affect far more than just income taxes – it can influence phaseouts, credits, and benefit eligibility. For consistent but modest givers, this is a meaningful change.

10. The New Senior Deduction (Age 65 and Older)

Taxpayers aged 65 and older, both those itemizing and claiming the standard deduction, may claim a new $6,000 deduction per qualifying taxpayer, phasing out at a six percent rate for those earning over $75,000 (single) and $150,000 (joint) as part of the separate senior deduction under the OBBBA. This is brand new and it’s a big one.

The new deduction for the 65-plus crowd is separate from the basic standard deduction and the bonus standard deduction for people 65 and older. Eligible taxpayers can claim the new deduction whether they take the standard deduction or itemize – but it’s offered only through the 2028 tax year. If you’re married and your spouse is also 65 or older, the maximum deduction is $12,000, but married couples must file a joint return to claim the deduction.

11. The No-Tax-on-Tips Deduction

This is one of the more talked-about provisions from the One Big Beautiful Bill, and for good reason. You can claim the tip deduction whether or not you itemize on your return. If you’re married, you must file a joint return to claim it. The deduction is available for tax years 2025 through 2028.

Tipped workers may be eligible to deduct up to $25,000 for qualified tips. You must have a Social Security number valid for employment on the day you file your return to be eligible for the tip deduction, overtime deduction, and senior deduction. If you work in hospitality, food service, or any tip-based industry, this deduction could genuinely change the numbers in your favor. It’s hard to say exactly how large the impact will be for every worker, but for some, it’s a significant chunk of their income that is now shielded.

12. The Qualified Overtime Deduction

The One Big Beautiful Bill created another new tax break for people who are still working – the overtime deduction. It allows workers to deduct up to $12,500 (or up to $25,000 for joint filers) in overtime compensation from their taxable income. The deduction is reduced by $100 for every $1,000 of MAGI over $150,000 ($300,000 for joint returns), eventually dropping to $0 if your MAGI is $275,000 or greater ($550,000 or greater for joint filers).

Like the deduction for tipped workers, the overtime deduction is available to both itemizers and taxpayers who claim the standard deduction. Married people must file jointly to qualify, and it’s offered only through the 2028 tax year. Let’s be real – if you’ve been grinding extra hours and watching that overtime money shrink in your paycheck, this deduction is the closest thing to financial justice the tax code has offered working Americans in years.

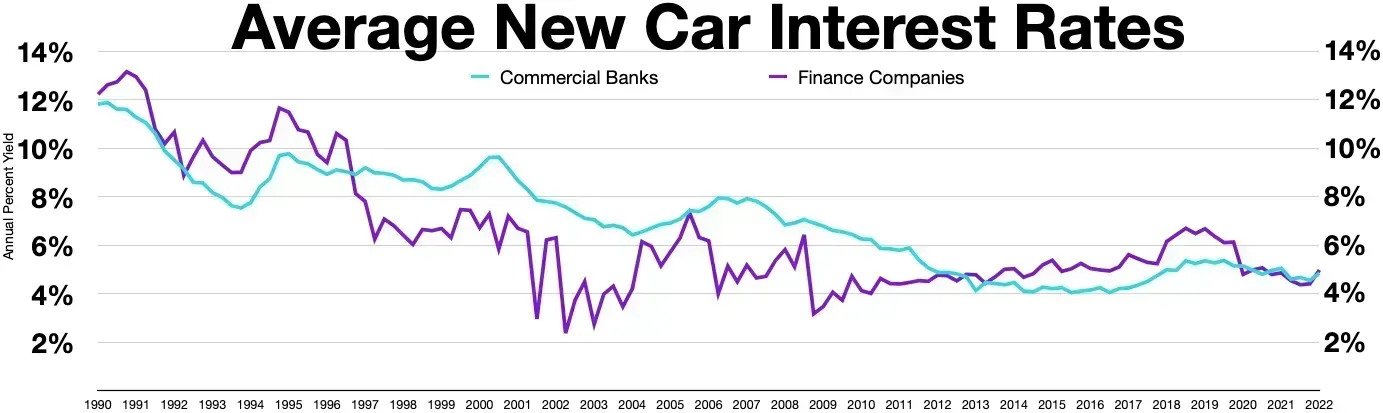

13. The New Car Loan Interest Deduction

The One Big Beautiful Bill Act added a car loan interest deduction temporarily available for tax years 2025 through 2028. The vehicle must be new and for personal use. It must have a final assembly in the United States. The loan must be secured by the vehicle and originated after December 31, 2024. The maximum annual deduction is $10,000. The deduction begins to phase out for taxpayers with a Modified Adjusted Gross Income over $100,000 for single filers and $200,000 for joint filers.

You can claim the car loan interest deduction whether or not you itemize, but the deduction is available only for the 2025 through 2028 tax years. Your lender was required to have provided a statement to you by January 31, 2026. indicating the total amount of interest you paid on your auto loan in 2025. All new or enhanced deductions are available for both itemizing and non-itemizing taxpayers. If you recently bought a new American-made vehicle with a loan, this deduction is one you absolutely don’t want to miss.