The New Definition of Comfortable: The Exact Net Worth Needed to Retire in the Top 10% Today

Let’s be real, the bar for a comfortable retirement keeps moving. What your grandparents needed to live well doesn’t even come close to cutting it anymore. The numbers have changed dramatically, and honestly, they might shock you more than you think.

The $1.8 Million Threshold That Changes Everything

The threshold to be in the top 10% of U.S. households by net worth grew from about $1.3 million to roughly $1.8 million over the last five years, largely due to rising stock and home values, according to a recent Visa analysis of 2024 U.S. Census Bureau survey data. That’s a roughly 40% jump in just five years. Between 2020 and 2024, the threshold for the top 10% of net worth grew about 40%, compared with about 23% for income, according to Visa’s analysis. What does this mean? Wealth has been growing twice as fast as paychecks.

The implications are staggering. The U.S. median home price rose about 25% over the last five years, per U.S. Census data, and the S&P 500 gained roughly 109%. If you weren’t invested in stocks or real estate during this period, you likely fell further behind. Think about it: those who already owned homes and had money in the market saw their wealth explode while everyone else watched from the sidelines.

What Retirees in the Elite Group Actually Have

To crack the top 10% of retirees, your net worth needs to hit around $1.9 million, according to Federal Reserve Board survey data. Here’s where things get interesting, though. Simply having that net worth isn’t enough to live like you’re wealthy. For those aged 65 to 69, the top 10% have an annual income of $200,000. Notice the gap? You need nearly two million in assets, yet these retirees are pulling in six figures annually.

They earn income from a combination of dividends, rental properties and strategic portfolios, which allows them to live comfortably without draining their principal savings. This is the crucial difference between being technically wealthy on paper versus actually living well in retirement. Many people think hitting a certain net worth is the finish line, when really it’s just the starting point. The real challenge is making that wealth work for you.

The Investment Strategy That Separates the Top 10%

A typical portfolio for someone in the top 10% might hold around 60% stocks, 35% bonds and just 5% cash or cash-like investments. This might surprise you because conventional wisdom tells retirees to play it safe. Here’s the thing: wealthy retirees don’t follow that advice. They’re still looking for growth even in retirement, rather than shifting entirely to conservative investments.

That approach works because they have enough cushion to weather market downturns. Meanwhile, those with smaller nest eggs feel pressured to park everything in safe, low-yield accounts that barely keep pace with inflation. The top 10% of Americans hold over 87% of corporate equities and mutual fund shares, with the value of those assets growing sharply since 2020, according to Federal Reserve data. This concentration means market gains disproportionately benefit those who were already wealthy, creating a self-reinforcing cycle.

Why Most Americans Are Nowhere Close

According to a Washington Post analysis of the Federal Reserve’s 2022 Survey of Consumer Finances, the median American family has a net worth of just $192,900. That’s less than one tenth of what’s needed to reach the top tier. Recent Federal Reserve data reveals a stark contrast: the average net worth for those aged 65 to 74 is $1,794,600, while the median is just $409,900. The gap between average and median tells you everything you need to know about wealth concentration in America.

The top 10% of Americans by net worth had a median retirement account balance of $900,000 as of 2022, while the average retirement account balance for the top 10% was close to $1.3 million in 2022. Remember, these are just retirement accounts, not total net worth. When you add real estate equity, business ownership, and other assets, the numbers climb even higher. Most Americans struggle to save anything close to these figures while managing everyday expenses, student debt, and healthcare costs.

The Reality Check Nobody Wants to Hear

According to the Northwestern Mutual Planning & Progress Study, “Americans’ ‘magic number’ to retire comfortably in 2025 is $1.26 million, $200,000 less than the $1.46 million reported last year and nearly flat with 2022 and 2023 estimates.” Interestingly, Americans actually lowered their expectations from 2024. Perhaps reality is finally setting in. The gap between aspiration and achievement has never been wider.

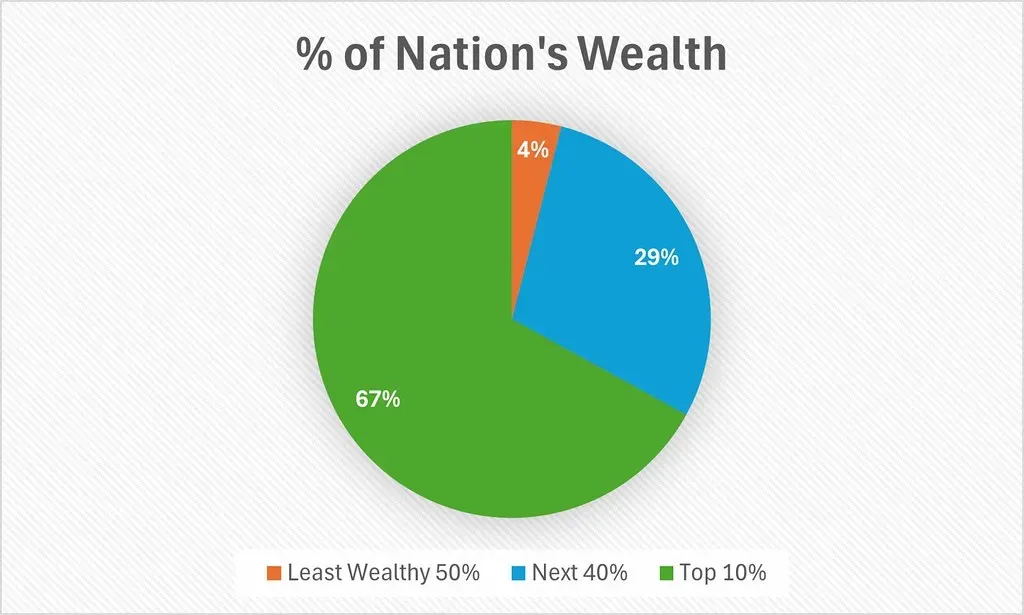

The top 10% of households by wealth had $8.1 million on average, and as a group, they held 67.2% of total household wealth. Meanwhile, the bottom 50% of households by wealth had $60,000 on average and as a group, they held 2.5% of total household wealth. These aren’t just statistics. They represent fundamentally different lived experiences and retirement realities.

The truth is uncomfortable but necessary: reaching the top 10% requires not just saving aggressively, but also strategic investing, favorable timing, and often some degree of privilege or luck. It’s achievable for some, but the math shows it’s increasingly out of reach for most. What do you think? Are these thresholds realistic goals or are they widening an already unbridgeable gap?