The Inheritance Gap: Why Most Millennials Won’t Receive the Windfall They Expect

The Stark Reality Behind Trillion-Dollar Promises

The so-called Great Wealth Transfer has become one of the most talked-about financial phenomena of our time, with projections suggesting that nearly $100 trillion will be transferred from Baby Boomers and older generations over the next few decades. Yet behind the staggering headlines lies a troubling disconnect between expectation and reality. One-third of Millennials expect to receive an inheritance, but only 22% each of Gen X and Boomers say they plan to leave a financial gift behind, according to Northwestern Mutual’s 2024 Planning & Progress Study. This expectation gap represents more than just miscommunication – it signals a fundamental misunderstanding about where boomer wealth will actually end up.

Healthcare Costs Are Devouring Retirement Savings

A healthy 65-year-old male retiring in 2024 was projected to spend approximately $281,000 on healthcare expenses during retirement, assuming a lifespan of 88 years, requiring $188,000 in savings in 2024 to cover these costs, according to the 2024 Milliman Retiree Health Cost Index. For women, those figures were even higher. A lot of Gen Xers may not get the inheritance they’re expecting to get because their parents encountered ballooning expenses in the later years of life, and the eye-popping figures surrounding the wealth transfer often obscure the reality that health care for the elderly is incredibly expensive and frequently wipes out people’s life savings, notes financial expert Greg McBride. The harsh truth is that nursing homes, assisted living facilities, and long-term medical care represent financial black holes that can consume decades of accumulated wealth in just a few years.

Long-Term Care Threatens Family Legacies

Genworth’s 2024 Cost of Care Survey found that the average cost of a semi-private room in a nursing home was $9,277 a month, while a private room cost $10,646 a month, and an assisted living facility cost nearly $5,900 a month. These expenses compound rapidly, and most Americans lack adequate insurance coverage to protect against them. Long-term care bills can significantly deplete a planned inheritance, especially when someone needs nursing home, assisted living facility, or in-home care for multiple years and doesn’t have a plan to pay for it, though policies can cover hundreds of thousands of dollars in care expenses. Without proactive planning through insurance or trusts, families watch helplessly as estates meant for the next generation instead flow directly to healthcare providers and facilities.

Boomers Prioritize Their Own Retirement Over Inheritances

The boomer generation has made its priorities clear, and leaving large inheritances isn’t at the top of the list. Only 11% of Boomers said leaving something for the kids is their top financial goal, while another 35% said it’s “very important” according to multiple studies. This represents a cultural shift from previous generations who viewed leaving an inheritance as a moral obligation. Although 35% of boomers said leaving something for the next generation was very important, only 11% indicated it was their top financial goal, revealing that boomers are increasingly embracing what some call the “spend the kids’ inheritance” philosophy. Rising concerns about retirement security, longer lifespans, and the desire to enjoy their golden years have fundamentally altered how this generation views wealth transfer.

Only the Wealthy Will Pass Down Significant Assets

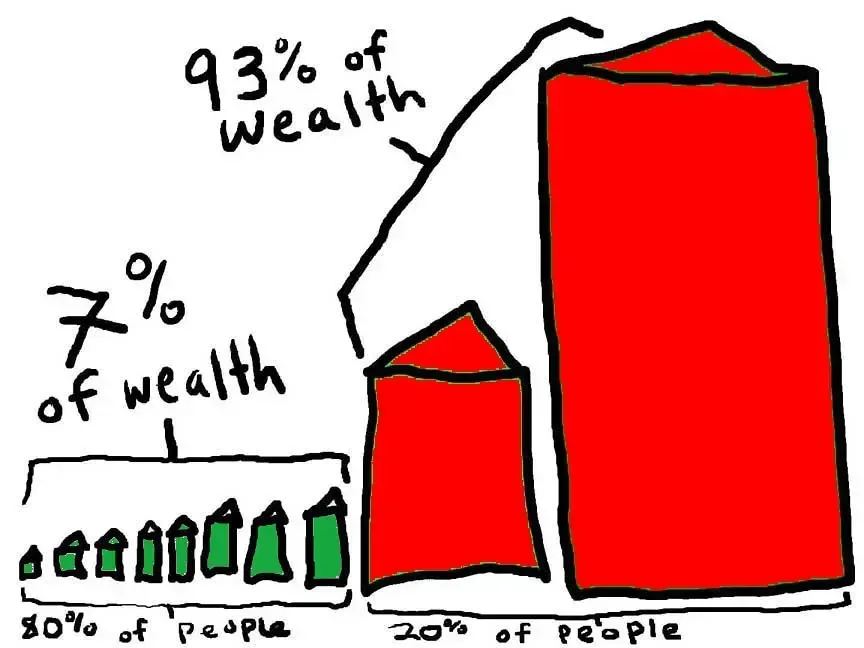

The wealth transfer narrative obscures a critical reality about inequality. Cerulli Associates estimates that 68% of the wealth transferred through 2045 will come from only 6.9% of U.S. households – the estimated number of households with at least $1 million in investable assets. This concentration means the vast majority of Americans will receive little to nothing. Just one-third of white families and about one in every 10 Black families receive any inheritance at all, and more than half of those inheritances will amount to less than $50,000, according to a Federal Reserve Bank of Boston study. The ultra-wealthy will indeed transfer enormous sums to their heirs, but this represents a tiny fraction of the population, leaving most millennials and Gen Z to build wealth through their own means.

Expectations Wildly Exceed Reality

The numbers tell a sobering story of misaligned expectations. 68% of millennials and Gen Zers have received or expect to receive an inheritance of nearly $320,000 on average, and 52% of millennials think they’ll get even more – at least $350,000 – however, 55% of baby boomers who plan to leave behind an inheritance said they will pass on less than $250,000, according to research from USA Today Blueprint and Alliant Credit Union. This gap of roughly $100,000 represents more than mathematical error – it reflects fundamental breakdowns in family communication about finances. Many adult children have built retirement plans, home purchase strategies, and debt payoff timelines around inheritances that will never materialize at the levels they anticipate.

Lack of Family Communication Creates False Hope

Part of the discrepancy is because “parents are just not communicating well with their adult children about financial topics,” and when you tack on inflation, high health-care costs and longer life expectancies, boomers suddenly may be feeling less secure about their financial standing – and less generous when it comes to giving money away, explains Isabel Barrow, director of financial planning at Edelman Financial Engines. This silence around money matters leaves younger generations planning their financial futures based on assumptions rather than facts. 90% of parents intend to leave an inheritance to their children but 48% do not have a specific plan in place, according to the Edelman report. Without open conversations and documented estate plans, families remain trapped in a cycle of unrealistic expectations and inevitable disappointment.

Spouses Will Inherit Before Children Do

Another overlooked reality complicates the inheritance timeline. Given an age gap between couples, spouses often outlive their other halves, meaning that for an average of four years, one individual will often inherit a sum of money before passing it on, with an estimated $9 trillion of wealth to be transferred intra-generationally – or horizontally – between spouses, according to UBS’s Global Wealth Report 2024. This means millennials waiting for inheritances from boomer parents may actually be waiting for their surviving parent to pass away, potentially delaying wealth transfer by a decade or more. During this extended period, healthcare costs continue to erode the estate, further diminishing what eventually reaches the next generation.

Millennials Must Rely on Themselves

The inheritance gap forces a difficult reckoning for millennials already facing economic headwinds. 38% of Gen Zers and 32% of Millennials expect an inheritance from their parents, and 54% of Gen Zers and 59% of Millennials reported that an inheritance is “crucial to achieving financial security and retiring in comfort” according to Northwestern Mutual research. This reliance on future windfalls represents dangerous financial planning. Walden said the Great Wealth Transfer is coming, but Gen Z and millennials shouldn’t rely on the death of a loved one to begin their wealth acquisition journey in earnest, noting “It’s hard to target when that’s going to come, so I would argue to any young person that I would be talking to, have a plan, be consistent with the plan”. Building wealth through consistent saving, strategic investing, and career advancement offers far more reliable security than counting on inheritances that may never arrive.

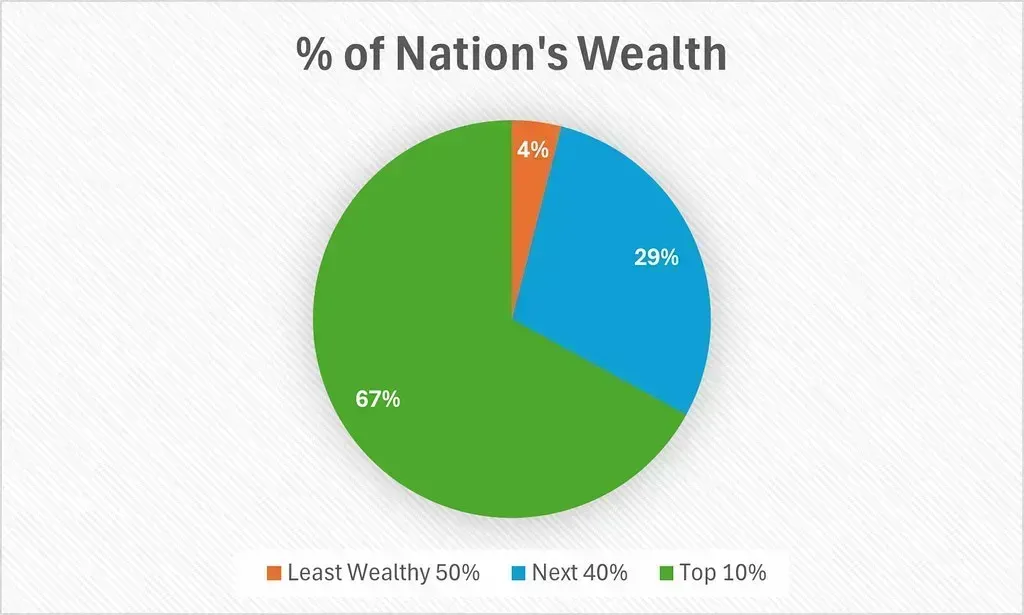

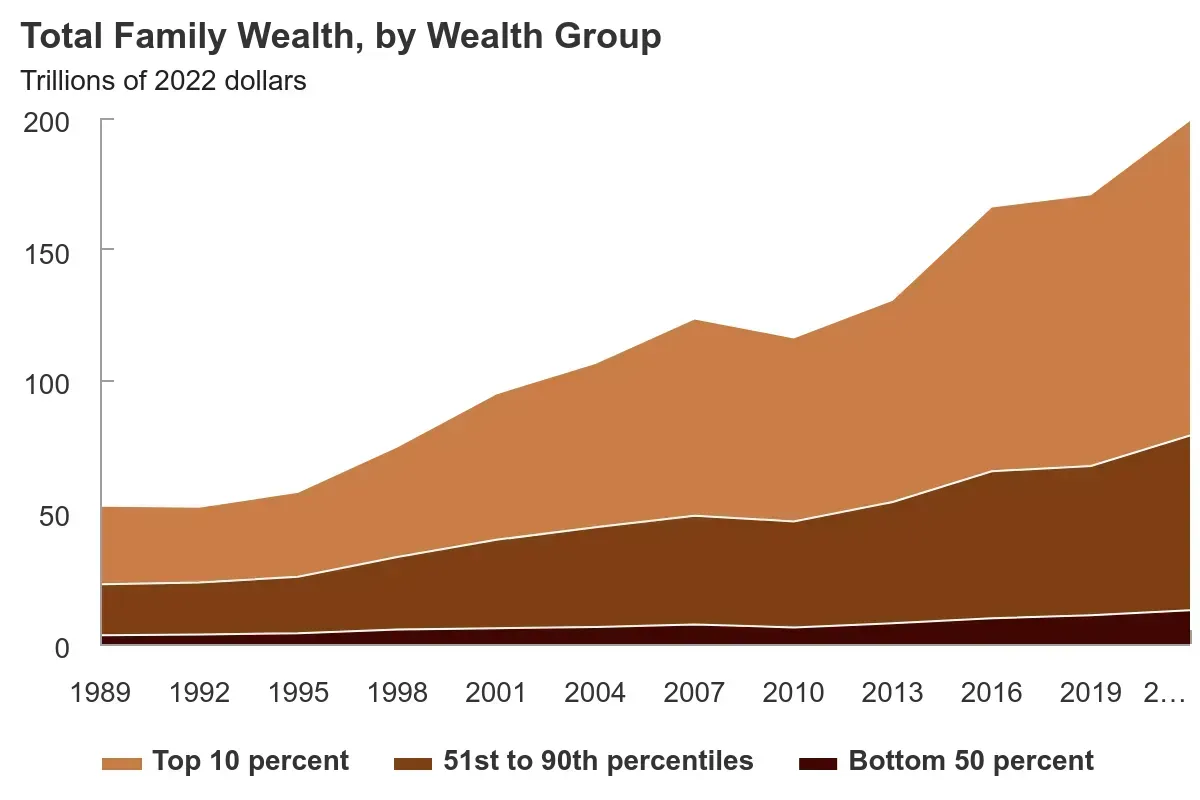

Wealth Inequality Will Deepen Among Millennials

The inheritance gap will exacerbate existing divisions within the millennial generation itself. With generational wealth amassing and creating large gaps in familial wealth between America’s richest and poorest households, additional endowments of assets from baby boomers will make the fortunate even more fortunate, as a study conducted by the Resolution Foundation revealed that wealthier boomers are more than two times as likely to leave inheritances to their children than poorer Americans, and cross generational wealth inequalities could become further ingrained in American society, creating further division. The millennials who do receive substantial inheritances will gain massive advantages in homeownership, business creation, and retirement security, while those without family wealth face increasingly steep barriers. This bifurcation creates what some researchers call a “millennial class war,” where birth circumstances rather than individual effort increasingly determine financial outcomes, fundamentally challenging the American narrative of meritocracy and self-made success.