The Net Worth Line That Now Defines “Affluent” in 2025

Here’s the thing about wealth in America right now. The old rules don’t really apply anymore. Having a million dollars in the bank used to be the golden ticket to being considered rich. That status symbol, that retirement dream so many people chased for decades, doesn’t carry the same weight it once did. Honestly, it’s hard to say for sure, but the financial landscape has shifted dramatically, and with it, the goalposts for what makes someone affluent have moved considerably further away.

So what does it actually take to be considered affluent these days? According to recent analysis from Visa Business and Economic Insights, you’re not truly affluent unless you’re sitting in the top ten percent of American households. The numbers behind that threshold might surprise you.

The New $1.8 Million Threshold That Separates Affluent From Everyone Else

Visa now defines affluent as entering the top ten percent of U.S. households, which requires an annual household income of $210,000 or higher, or a net worth of at least $1.8 million. That’s according to December 2024 analysis based on recent U.S. Census survey data. Think about that for a second. Nearly two million dollars just to crack the top ten percent.

These thresholds have increased since 2020, when the income needed to reach the top ten percent was roughly $170,000 and the wealth cutoff sat around $1.3 million nationally, with rising home values and stock prices pushing both numbers higher. The threshold for households to be in the top ten percent of earners rose roughly a quarter since 2020, according to Visa’s research.

What caused this leap? Let’s be real, it wasn’t just inflation. This shift is driven by two key factors: a surge in asset prices that has elevated the net worth required, and persistent labor shortages that have fueled strong income growth. The combination of skyrocketing real estate values and a booming stock market through 2024 created an environment where wealth accumulation at the top accelerated faster than most people could keep pace with.

How Geography Completely Reshapes The Affluence Game

Where you live matters more than you might think when it comes to crossing the affluence threshold. U.S. average requirements stand at $210,000 in income and $1.8 million in net worth, but regional variations paint a dramatically different picture, with the West requiring income of $227,000 or more and net worth exceeding $2 million. The Northeast follows close behind with similar barriers.

The South is the clear leader, home to the largest share of affluent households at four million and the highest share of affluent spending at roughly one third, with the region’s more affordable housing, lower taxes, and robust job growth making it a magnet for affluent baby boomers, Gen Xers, and millennials. Meanwhile, the Midwest, despite having the lowest affluence benchmarks, lags all other regions in affluent footprint and spending, reflecting its lower cost of living and heavier reliance on manufacturing and agriculture.

This creates some fascinating dynamics. Someone earning $205,000 in Atlanta might be considered affluent, while that same person in San Francisco barely makes the cut. The cost of living differences aren’t just slight variations, they’re fundamental reshaping forces that determine whether your household wealth translates into actual affluence.

Why The Million Dollar Mark Lost Its Meaning

The classic milestone of a $1 million net worth isn’t what it used to be. Seriously, think about what a million dollars meant in 1990 versus what it means now. According to Charles Schwab’s surveys, Americans think it takes an average of $2.3 million to be considered wealthy in 2025, which is a slight drop year over year but consistent with the five year trend.

There’s a massive gap between what people think makes you wealthy and what actually puts you in the affluent category. In 2024, Americans stated that the average net worth they consider wealthy is $2.5 million, according to Charles Schwab’s annual Modern Wealth Survey which surveyed 1,000 Americans, up slightly from $2.2 million compared with the previous year. Yet the actual threshold to be in the top ten percent is lower at $1.8 million in net worth.

Here’s what’s really happening. In 2024, high net worth households, those with at least $5 million in financial assets, were estimated to control $49 trillion of financial wealth, or roughly half of the overall total, with this group now at 3.4 million households including more than 100,000 ultra high net worth households with financial wealth exceeding $50 million, according to Cerulli Associates. The concentration of wealth at the very top is pulling away from everyone else.

The Real Median American Versus The Affluent Dream

Let me paint the actual picture of where most Americans stand financially. The average net worth of Americans is roughly $1.06 million, while the median net worth of American households is $192,900, according to the Federal Reserve’s 2022 Survey of Consumer Finances released in 2023. That massive gap between average and median tells you everything about wealth concentration.

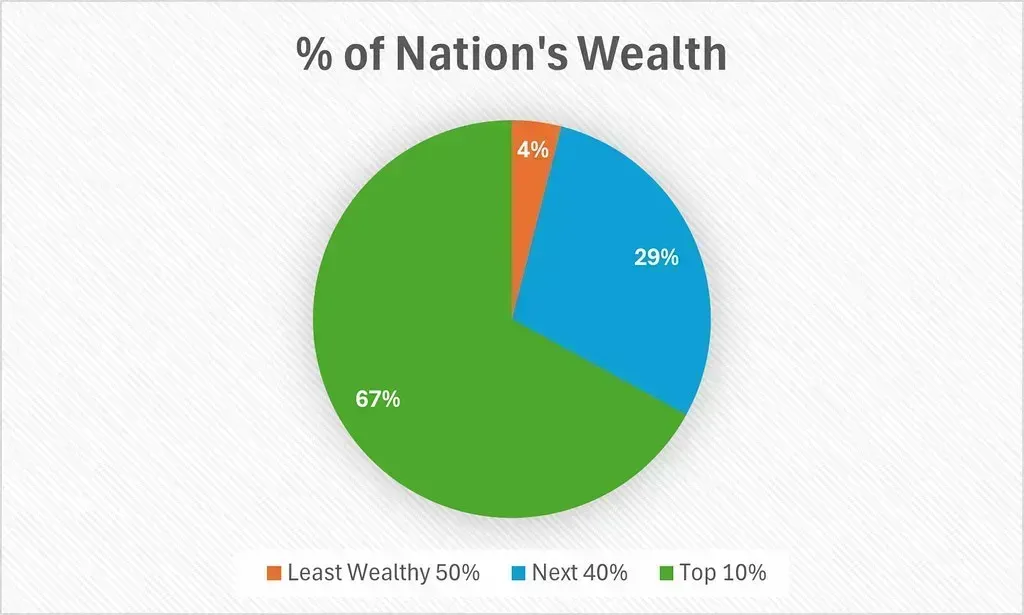

For the fourth quarter of 2024, the top ten percent of households by wealth had $8.1 million on average and as a group held roughly two thirds of total household wealth, while the bottom fifty percent of households by wealth had $60,000 on average, according to Federal Reserve data. The chasm is staggering.

Nearly sixty percent of households in the U.S. have a net worth of $100,000 or more after accounting for debts, with roughly thirty percent having a net worth of $500,000 or more, according to SmartAsset’s 2025 study. So when we’re talking about an affluence line of $1.8 million, we’re discussing a threshold that roughly ninety percent of American households haven’t crossed. The aspiration feels increasingly distant for families just trying to build some basic financial security.

Who Actually Makes Up Today’s Affluent Class

While Gen X comprises the largest group of affluent households at approximately fifty seven percent, it’s the baby boomers who are spending the most, with affluent boomers making up just twelve percent of affluent households but accounting for a staggering forty two percent of all affluent spending, as they control the bulk of their generation’s wealth and fund discretionary pursuits like travel and dining through investment income and dividends, according to Visa’s research.

This creates some interesting market dynamics. Affluent households allocate a larger share of their budget toward discretionary purchases, spending roughly $180 more per month than non affluent consumers on apparel, and restaurant spending for an affluent consumer peaks at age 50 compared to age 39 for non affluent consumers. The spending power differential extends well into later life stages.

In 2024, the global high net worth individual population rose by roughly three percent, driven by gains in the ultra high net worth segment, with North America seeing the strongest growth and the U.S. adding approximately 562,000 new millionaires, bringing its total to about 7.9 million individuals with at least $1 million in liquid assets, according to recent wealth reports. The affluent class continues expanding, but the bar to entry keeps rising.

The affluence threshold reflects something deeper than just numbers on a balance sheet. It captures how dramatically the cost of maintaining an upper middle class lifestyle has escalated, how geographic location can make or break your financial standing, and how the concentration of wealth at the very top continues reshaping what it means to be financially comfortable in America. Are these thresholds sustainable, or will they keep climbing beyond reach for most households? Only time will tell, but right now, $1.8 million is the number that separates affluent from everyone else.