Medicare Part B Trap: The One Document You Must File at 65 to Avoid Lifetime Penalties

Turning 65 should be a milestone worth celebrating, not a financial mistake that haunts you forever. Yet thousands of Americans unknowingly trigger a Medicare trap every year that costs them hundreds of extra dollars each month for the rest of their lives. The culprit? Missing one critical enrollment deadline or failing to file the right paperwork at the right time. Here’s the thing: Medicare doesn’t send reminder letters, and the penalties are permanent. So what document could possibly be that important?

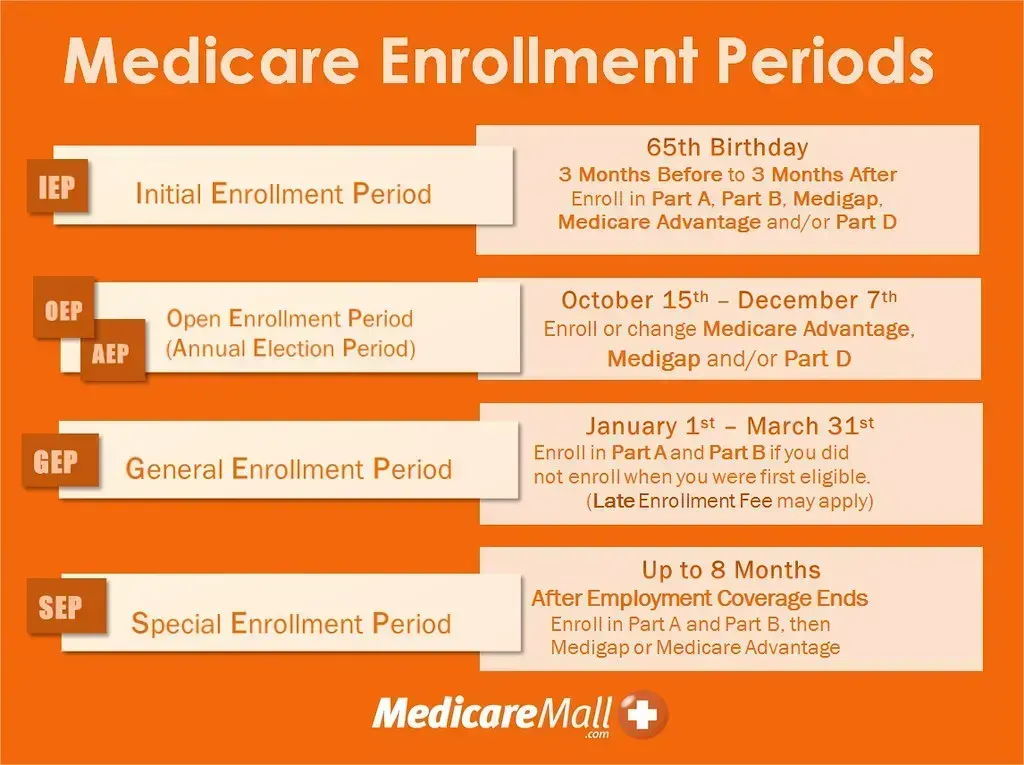

The Seven-Month Window That Determines Your Financial Future

Your Initial Enrollment Period for Medicare begins three months before the month you turn 65 and ends three months after your birthday month. This seven-month window is your golden opportunity to enroll without consequences. Miss it, and you’re looking at trouble. For each 12-month period you delay enrollment in Medicare Part B, you’ll pay a 10% premium penalty, and that’s not a one-time fee. In most cases, you will have to pay that penalty every month for as long as you have Medicare. Let’s be real: that could mean paying an extra charge for twenty or thirty years.

Form CMS-40B: Your Shield Against Permanent Penalties

If you’re still working past 65 with employer coverage or have other special circumstances, Form CMS-40B is used if you already have Medicare Part A and want to sign up for Part B during a Special Enrollment Period. This document is crucial. You need to complete CMS-40B and CMS-L564, then upload your evidence of Group Health Plan or Large Group Health Plan coverage based on current employment. The CMS-L564 form is particularly important because your employer fills it out to verify you had creditable coverage, essentially proving you had a legitimate reason to delay Medicare.

Think of these forms as your get-out-of-jail-free card. Without them, Medicare assumes you simply forgot or chose not to enroll, and the penalties kick in automatically.

The Shocking Statistics Behind Late Enrollment Mistakes

In 2021, an estimated 779,400 Medicare beneficiaries were paying the Part B late enrollment penalty, with the average penalty increasing their monthly premium by nearly 30%. That’s not a small group of forgetful people. One study estimates that about 20% of people paying the Part B penalty did not know about these penalties at the time they reached age 65. The numbers get even more disturbing when you look at who’s affected most. The share of penalty-payers was higher among American Indian/Alaska Native enrollees at nearly three percent, Hispanic/Latino at roughly two percent, and Asian/Pacific Islander and Black enrollees compared to White enrollees.

In 2021, the portion of Part B enrollees paying a penalty ranged from less than one percent in Indiana to over three percent in the District of Columbia. In Puerto Rico, the rate jumped to nearly five percent.

How the Math Works Against You Forever

The penalty calculation is brutally simple and ruthlessly permanent. Since the base Part B premium in 2026 is $202.90, if you delayed enrollment for seven years your monthly premium with the penalty will be $344.93. Let me break that down: you’d be paying an extra hundred and forty dollars every single month. Over twenty years, that’s nearly thirty-four thousand dollars in penalty fees alone. If you waited 2 full years to sign up for Part B and didn’t qualify for a Special Enrollment Period, you’ll have to pay a 20% late enrollment penalty plus the standard Part B monthly premium.

The penalty compounds over time too, because it’s based on a percentage. Since Part B premiums usually rise each year, your late enrollment penalty usually rises as well.

When You Actually Have Protection From Penalties

Not everyone needs to panic about the 65 deadline. If you actively work for a large employer who has 20 or more employees and are enrolled in their group health plan, then you have creditable coverage for Medicare. This is huge. If you or your spouse is still working and has healthcare coverage through an employer, you can wait to sign up for Part B without paying a penalty, but once your employer coverage ends, the only way to avoid a penalty is to enroll during an 8-month Special Enrollment Period.

However, small employer plans don’t count. A small employer is an employer who has fewer than 20 employees, and small employer group health plans are not creditable coverage for Medicare. COBRA coverage doesn’t protect you either. Having retiree health benefits or COBRA extended coverage from a former employer after age 65 will not exempt you from Part B late penalties.

The Automatic Enrollment Myth That Costs People Thousands

Many Americans assume Medicare enrollment happens automatically when they hit 65. That’s only partially true, and the confusion causes massive problems. While most older adults are automatically enrolled in Medicare Part B because they are receiving Social Security benefits at age 65, a growing number are not. In 2016, only 60% of Medicare-eligible 65-year-olds were taking Social Security, compared to 92% in 2002.

More older adults are working later in life and deferring Social Security, though they may not realize that doing so impacts their Medicare enrollment and coverage. This trend is creating a perfect storm for enrollment mistakes. People think they’re being financially savvy by delaying Social Security to increase their eventual benefit, but they don’t realize they’re missing their Medicare window.

Special Enrollment Periods: Your Second Chance Options

Let’s say you’ve already missed your Initial Enrollment Period. You might still have options. If, due to an exceptional condition, you didn’t sign up for Medicare Premium Part A or Part B during your Initial Enrollment Period, General Enrollment Period, or a Special Enrollment Period you were previously eligible for, you can sign up without a late enrollment penalty during a SEP for Exceptional Conditions. What qualifies as exceptional? Some common reasons for qualifying include being impacted by a natural emergency or disaster, losing Medicaid coverage, or being released from jail.

If you did not enroll in Part B during your enrollment period due to misinformation provided by your employer, group health plan, or agent or broker, you may qualify for a Special Enrollment Period. You’ll need documented evidence or a written attestation about the misinformation.

The Hidden Cost Beyond the Premium Penalty

The financial penalty isn’t the only consequence of missing your enrollment window. There’s also a gap in coverage that could devastate your finances. After your Initial Enrollment Period ends, you can only sign up for Part B during the General Enrollment Period between January 1 and March 31 each year, and your coverage starts the month after you sign up. Imagine needing a major surgery in May but having to wait until the following January to even apply for coverage that won’t start until April. You’d be facing those medical bills entirely on your own.

I think one of the cruelest aspects of this system is how it punishes honest mistakes as harshly as deliberate avoidance. The federal government doesn’t distinguish between someone who genuinely didn’t know and someone who gambled on staying healthy.

How Employers Often Give Terrible Medicare Advice

Human resources departments often give out bad advice about Part B, according to Medicare enrollment experts. Your well-meaning HR representative might tell you to wait, not realizing your company doesn’t have enough employees for your plan to qualify as creditable coverage. Unfortunately, you can’t get equitable relief if you were misadvised by your employer. Only misinformation from the federal government itself can potentially get penalties waived.

If you find yourself without Part B coverage or are paying a penalty because you received bad advice from the federal government, Social Security may be able to waive your Part B penalty, enroll you into Part B, or do both things. The key word there is “may.” There’s no guarantee, and the burden of proof falls on you.

Why This System Desperately Needs Reform

The bipartisan BENES 2.0 Act would require Medicare to alert people approaching eligibility about the actions they must take and the deadlines they must meet. This information could reduce the number of people who incur late-enrollment penalties because of mistakes. It sounds like common sense, doesn’t it? Yet as of 2026, it still hasn’t become law. Because Medicare enrollment rules are so complex, many people end up paying the penalty due to honest error.

Currently, half of all people with Medicare – over 30 million older adults and people with disabilities – have annual incomes below thirty-six thousand dollars. For these beneficiaries, a lifetime penalty of several thousand dollars per year represents a crushing financial burden. The system seems designed to trap people rather than help them.

Honestly, the entire structure feels less like a safety net and more like a minefield. The document you need depends on your specific situation, the deadlines vary, and the penalties are severe and permanent. What’s missing is a simple, proactive notification system that reaches people before they make irreversible mistakes. Until that changes, your best defense is knowledge and vigilance at age 65.