The Net Worth Americans Think They Need by 45 vs. the Real Number

The Magic Number: What Americans Think They Need

Americans believe it takes $839,000 to be “financially comfortable,” according to Charles Schwab’s 2025 Modern Wealth Survey, an increase from $778,000 reported last year, but down from the $1 million Americans cited in 2023. This fluctuating figure reflects the constant tension between rising costs and shifting economic realities. The 2025 response of $2.3 million for being “wealthy” was down from $2.5 million in 2024, though 63% of respondents said it takes more money to be wealthy this year than last, citing inflation, the cost of living and increased interest rates.

The Reality Check: What People Actually Have

The median net worth for Americans ages 45 to 54 in 2022 was $247,200. That number sits far below what most people think they need for financial comfort. As of 2022, the average net worth of Americans was $975,800 for ages 45 to 54. The massive gap between median and average figures reveals how wealth concentration skews our understanding of what’s normal.

Why the Numbers Are So Far Apart

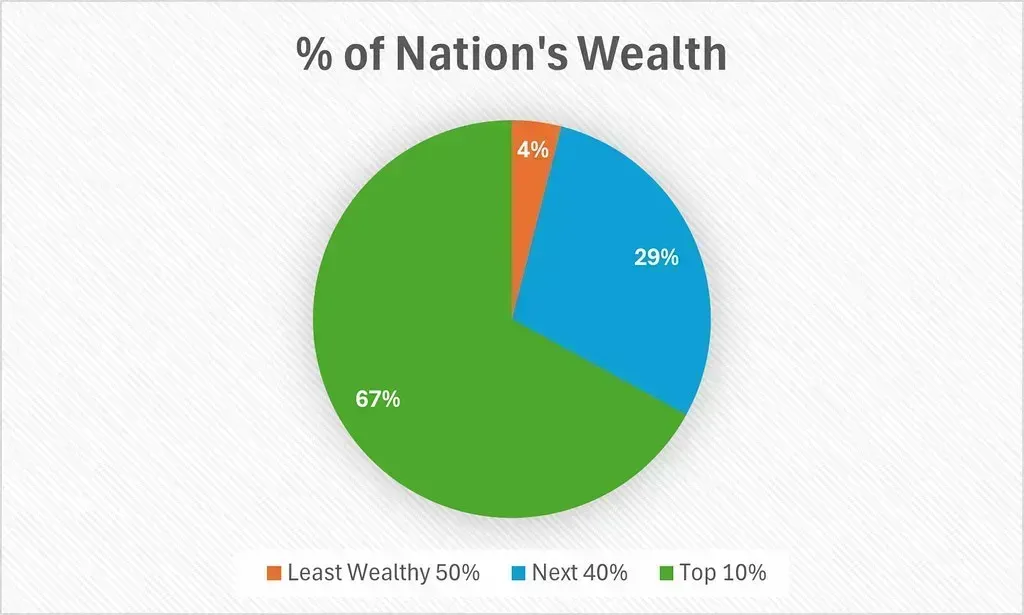

Median figures are far lower than averages, highlighting how a few high-wealth households skew results, with the average net worth in the 50s at $1,369,809, but the median only $192,964, meaning half of households in that age range have less than $192,964 in net worth. Think about it like this: if you walk into a room with nine regular folks and Jeff Bezos, suddenly everyone in that room is a billionaire on average. The median tells you what the person in the middle actually has, which is a far more useful benchmark.

What Financial Experts Say You Should Have

By age 45, financial experts typically recommend having saved 3-6 times your annual salary for retirement, with about four times your annual salary tucked away by this age as a helpful guideline. As a general rule of thumb, you’ll want to have saved around four times your salary by age 45. So if you’re pulling in roughly sixty thousand dollars a year, you’d ideally have somewhere between two hundred and three hundred thousand dollars saved up. Most people aren’t hitting that target, though.

The Psychological Gap Between Comfort and Reality

The average American says you need $839,000 to feel financially comfortable, meaning stopping the constant worry about bills and basic expenses, while this gap between comfortable and wealthy shows that most people understand wealth as something far beyond mere financial security. There’s something revealing about that distinction. Financial comfort isn’t about buying yachts or luxury cars; it’s about sleeping soundly without worrying if an unexpected car repair will derail your budget. Despite this philosophical evolution, 63% of people say it takes more money to feel secure this year than it did last year, with higher mortgage rates and the rising cost of essential goods continuing to drive up the practical requirements for financial peace of mind.

Generational Differences in Expectations

Gen Z survey respondents said they think that $329,000 is sufficient to be financially comfortable and $1.7 million is the amount needed to be considered wealthy, while Millennials said that a net worth of $847,000 will make you financially comfortable and $2.1 million would be considered wealthy. For GenX, the amount of money needed to be financially comfortable is $783,000, while boomers had the highest expectations, feeling that you need $943,000 to be financially comfortable and $2.8 million to be considered wealthy. Boomers, who’ve lived through more economic cycles, seem to have the most grounded expectations.

The Peak Earning Years Reality

Peak earning years are generally between 45 and 54, but you can grow your net worth by prioritizing earning, saving, repaying debts and investing over spending. Here’s the thing: your forties should be when everything clicks financially. You’ve got experience, your salary has climbed, and hopefully you’re not making the rookie mistakes from your twenties anymore. U.S. residents ages 45 to 54 have an average $313,220 in retirement savings. That’s encouraging, but still represents less than half of what people think they need for comfort.

How Assets Actually Build Up

As of October 2025, the average net worth was $770,892 for those in their 40s, rising from $321,549 in their 30s and increasing to $1,369,809 in their 50s. The median household net worth has increased 37% since 2019, after inflation, the sharpest increase recorded in the history of the survey. That jump largely came from housing market gains and stock market growth during the pandemic years. Real estate and retirement accounts form the backbone of most Americans’ wealth, not flashy investments or side hustles.

The Actual Path to Getting There

Consider automating your retirement contributions so they happen before you have a chance to spend that money elsewhere, and each time you receive a raise or bonus, consider directing at least a portion toward retirement before lifestyle inflation sets in, as increasing your contribution rate by just 1% annually can make a substantial difference over time. Small moves compound over decades. Research suggests it’s a good idea to try to save at least 15% of your income annually, including any employer contribution, as saving 15% can help you accumulate 10x your income by age 67. Honestly, most people struggle to save even ten percent consistently.

Where You Actually Stand

If your net worth sits around $2-$3 million, most Americans would consider you wealthy by 2026 standards and you’re also objectively in the top 10% of households, putting you well above the vast majority of the population, meaning you’ve achieved what most define as financial success. A net worth between $800,000 and $1 million places you in “comfortably financially secure” territory, representing true financial independence for many families, even if it doesn’t match the psychological threshold of wealth. The real question becomes: are you chasing a number or chasing peace of mind? Those two things aren’t always the same. What do you think matters more?