Why the Wealthy Avoid Putting Their Money Into a 401(k) – And What They Choose Instead

When you’ve climbed the income ladder far enough, the game changes. The retirement strategies most people rely on suddenly look limiting. For 2025, 401(k) plans allow all income levels to contribute, with IRS-employer match limits set at $350,000, yet this ceiling feels absurdly low when your annual compensation stretches well past seven figures. Let’s be real: if you’re earning several million a year, socking away roughly twenty-three thousand in pre-tax savings feels almost trivial, doesn’t it?

The truth is, many wealthy individuals don’t entirely avoid 401(k) plans, but they rarely rely on them as primary wealth-building vehicles. They’ve discovered alternative paths that offer greater flexibility, higher contribution thresholds, and more sophisticated tax advantages. What works for middle America doesn’t necessarily work when your net worth crosses eight or nine figures.

Contribution Limits Feel Like Handcuffs

In 2025, the IRS has increased the contribution limits for 401(k) plans. Individuals under 50 can now contribute up to $23,500, up from $23,000 in 2024. That sounds generous until you compare it to what the ultra-wealthy actually want to shelter from taxation. The 401(a)(17) rules only allow super-savers in 2025 to receive 401(k) contributions from their employers with consideration up to the first $350,000 of income for a qualified retirement plan.

Here’s where it gets frustrating for high earners. The IRS specifies that only the first $350,000 of an employee’s income can be considered for salary deferral into 401(k) plans, which means that both company and employee deferrals are often prohibited once an employee reaches that threshold. Think about someone earning five million annually. They’re effectively locked out from meaningful contributions relative to their income. The percentage they can save becomes almost comically small.

Alternative Investments Dominate Wealthy Portfolios

Research shows a stark divide in how different wealth tiers allocate capital. Among ultra-high-net-worth investors (those with a net worth of at least $30 million), alternative investments make up 20% of assets, compared to almost 0% for the average investor. That’s not a typo. While typical savers stuff money into traditional stocks and bonds within their workplace plans, the wealthiest fifth of Americans pours capital into private equity, hedge funds, and real estate deals.

Adoption of alternatives rises sharply with higher net worth: 39% of investors with $1–5 million report using alternatives, rising to 63% for households with $5–10 million, 80% for investors with over $10 million, and 91% for those above $20 million, according to a Goldman Sachs survey conducted in 2025. These aren’t accessible through standard 401(k) menus. The flexibility simply isn’t there. Alternative assets offer potentially outsized returns that traditional equity funds can’t match, especially during volatile market periods.

Private Placement Life Insurance Offers Tax Shelter Benefits

One vehicle gaining scrutiny and popularity among the ultra-rich is private placement life insurance. The investigation found that the domestic PPLI industry is now a tax shelter made up of at least $40 billion in policies held by only a few thousand individuals, who have net-worths reaching into the hundreds of millions or billions of dollars, according to a 2024 Senate Finance Committee report.

PPLI is primarily designed to help very wealthy people pay less taxes on their investments. PPLI was designed for people who want to invest in hedge funds but avoid the high taxes that come with those investments. The structure allows policyholders to invest in nearly anything – from private equity to real estate – while the growth remains tax-deferred inside the insurance wrapper. PPLI policies typically require minimum premium commitments of $1 to $2 million or greater (not including fees and other administrative costs), placing them firmly outside reach for average savers.

Defined Benefit Plans Blow Past 401(k) Ceilings

Business owners and self-employed professionals have another powerful tool that dwarfs 401(k) contributions. These plans provide large tax-deductible contributions averaging $100,000+ annually. Unlike the defined contribution structure of a 401(k), defined benefit plans calculate required annual funding based on a promised retirement income stream.

A personal defined benefit plan may be best for professionals age 50 or over who can make annual contributions of $90,000 or more for at least five years and who have few, if any, employees. I’ve seen cases where business owners in their late fifties contribute north of $200,000 annually. A few years ago a business owner and his spouse were able to deduct nearly $900,000 in a single year all on a tax-deferred basis using a newly established defined benefit plan. This individual was in his early 60’s and about 5 years away from his anticipated retirement. That kind of wealth acceleration simply isn’t possible with traditional workplace retirement accounts.

Wealthy Investors Value Flexibility Over Structure

The customization factor can’t be overstated. Policyholders are not limited to a predefined set of investment options; instead, they can work with their advisors to tailor their investment portfolio within the policy. This flexibility allows investors to align their investments with their risk tolerance, investment horizon, and overall financial goals. From equities and bonds to alternative investments like hedge funds and private equity, PPLI can accommodate a wide range of assets.

Compare that to the average 401(k) participant. In 2024, the average Vanguard plan offered 27.6 investment choices, typically limited to mutual funds and target-date funds. Wealthy investors want direct access to pre-IPO companies, distressed debt opportunities, and structured products. The 401(k) architecture simply wasn’t built for that level of sophistication. When you’re managing generational wealth, cookie-cutter investment menus feel restrictive.

Roth Conversions and Backdoor Strategies Still Matter

High earners haven’t entirely abandoned traditional retirement account structures – they’ve just learned to manipulate them more effectively. Such accounts have no income phaseout limits, so you can generally contribute the lesser of your income or $23,500 for 2025 (plus an additional $7,500 if you are 50 to 59 or 64 or older, or $11,250 if you are 60 to 63) to a traditional 401(k), according to Charles Schwab.

The Roth 401(k) option has become particularly valuable. Like their traditional 401(k) counterparts, Roth 401(k)s don’t have income phaseouts. So even if you don’t qualify for a Roth IRA because your income is above IRS limits, you can make after-tax contributions to a Roth 401(k). Sophisticated wealth advisors layer these vehicles together – maxing out employer plans, then funneling additional capital into backdoor Roth conversions and mega backdoor Roth strategies that can move hundreds of thousands into tax-free growth accounts annually.

Estate Planning Drives Alternative Vehicle Adoption

PPLI policies are actively promoted to ultra-wealthy Americans as tax-free hedge and private equity fund investments. PPLI policies are actively promoted to millionaires and billionaires as a way to transfer significant wealth to their heirs while bypassing income, gift and estate taxes. When your concern shifts from personal retirement security to multigenerational wealth transfer, the limitations of a 401(k) become even more apparent.

Death benefits from life insurance pass tax-free to beneficiaries, creating a powerful estate planning mechanism. Wealthy individuals are likely to exceed federal and state estate tax thresholds. Additionally, you may be able to help provide more wealth to your heirs tax-free while living by tapping into cash value. The ability to access policy cash value through loans during your lifetime while preserving a death benefit for heirs offers flexibility that qualified retirement plans simply can’t match.

The Wealthy Prioritize Liquidity and Control

Here’s something most people overlook: penalty-free access to capital matters tremendously to high-net-worth individuals. Traditional 401(k) plans lock your money away until age 59½, with limited exceptions. While a fifth of net worth remains in cash for preservation and flexibility, 80% of individuals with over $10 million in investable assets utilize alternatives, compared to 39% for those with $1–5 million.

This cash buffer provides optionality. Business opportunities arise. Market dislocations create once-in-a-decade buying chances. Having significant capital trapped in retirement accounts feels counterproductive when you’re actively building wealth rather than simply preserving it. The ultra-wealthy view liquidity as a strategic weapon, not a four-letter word. They’re willing to pay for structures that give them control over timing and deployment of capital.

Tax Law Changes Push Creative Planning

Recent regulatory shifts have made high earners even more creative. The IRS issued new regulations last month to implement a provision of a 2022 law known as the SECURE 2.0 Act, which requires that high earners who earned $145,000 or more in gross income as an individual the prior year make 401(k) catch-up contributions to after-tax Roth accounts starting with the 2026 tax year. This strips away the immediate tax deduction many professionals relied upon.

For example, if you earned more than $145,000 (as indexed for inflation) in 2025, you must make Roth catch-up contributions for 2026, which don’t provide an upfront tax break but can grow tax-free. Starting in 2026, higher earners must make 401(k) catch-up contributions to after-tax Roth accounts, which don’t provide an upfront tax break but the funds can grow tax-free. While Roth growth has advantages, losing the upfront deduction pushes wealthy savers toward vehicles where they maintain more control over the tax timing of their savings strategies.

What This Means for the Rest of Us

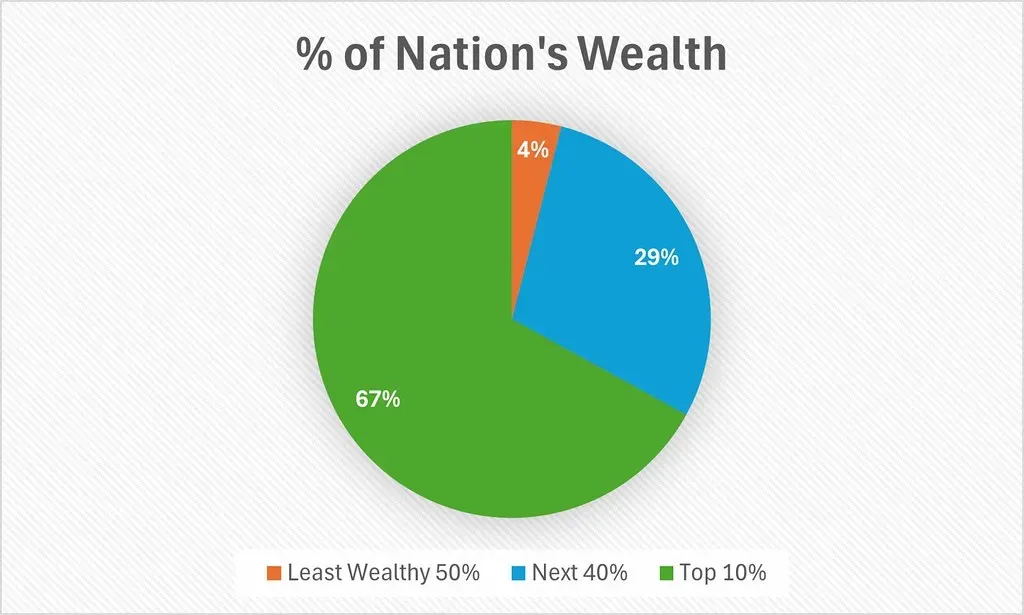

The gap between how wealthy individuals save and how middle-class Americans save continues widening. By 2024, the wealthiest 10% of Americans held nearly 27 times more wealth than the bottom 50%, according to Federal Reserve data. Access to sophisticated financial structures creates a compounding advantage that’s difficult to overcome through traditional savings alone.

Should we be concerned that PPLI represents just 0.003 percent of all individual life insurance policies in force in the United States, yet shelters tens of billions? Perhaps. The structures wealthy individuals use aren’t inherently wrong – many follow the tax code precisely as written. The real question becomes whether our retirement savings system should be reformed to offer more equitable opportunities across income levels, or whether these gaps are simply the inevitable result of differentiated earning power and access to specialized advice.

What’s clear is this: relying solely on a 401(k) is something the wealthy simply don’t do. They’ve built diversified architectures combining defined benefit plans, private insurance products, alternative investments, and tax-optimized account layering. The 401(k) might make a cameo appearance in their overall plan, but it’s never the star of the show. For anyone serious about building substantial wealth, understanding what the top tier does differently offers valuable lessons – even if all the tools aren’t immediately accessible.