Are You Above or Below Average? The Real Net Worth of a 71-Year-Old in America

Here’s the thing, when you hit your seventies in America, the question isn’t just about how much money you’ve saved. It’s about understanding where you really stand compared to everyone else at this stage of life. Honestly, the numbers can surprise you.

The highest average American net worth belongs to those aged 65 to 74 at $1,794,600, according to data from the Federal Reserve’s 2022 Survey of Consumer Finances. That sounds impressive, right? Yet here’s where reality hits differently. The median net worth of Americans between 65 and 74 was about 11 times higher at $410,000 than younger groups, which gives us a more honest picture of what most people actually have.

Why the Average Number Misleads Most People

Let’s be real about this. When financial experts throw around average figures, they’re often painting an overly rosy picture.

Median figures are far lower than averages, highlighting how a few high-wealth households skew results. For instance, for ages 55-64 the average net worth is $1,566,900, but the median is only $364,270. That gap tells you something crucial. The wealthiest households pull the average way up, making everyone else feel like they’re falling behind when they might actually be doing just fine.

Average wealth can be skewed by a few uber-wealthy individuals, while median net worth better represents the middle-of-the-road consumer. For example, the median net worth in 2022 was $192,900, a 37% increase over the previous three years. The average net worth, however, rose to a whopping $1,063,700. See the disconnect?

What Does a 71-Year-Old Actually Own

So what does someone at age 71 typically hold in their financial portfolio? Net worth then begins to decline gradually in the 70s ($1,462,121) and beyond based on Empower data from October 2025. Still, that’s the average talking again.

Americans in their 70s have an average retirement savings balance of $1,020,318; the median is $436,144, which represents just the retirement accounts. Home equity plays a massive role too. The median home equity for a senior homeowner age 65+ is $250,000, according to recent research. That’s nearly half the wealth picture for many older Americans.

Think about it. Roughly four out of five older Americans own their homes, and for many, that house represents the bulk of what they’ve built over a lifetime. Among homeowners ages 62 and older, home equity composed 81 percent of total net worth for Black homeowners and 89 percent for Latine homeowners, compared with 47 percent for white homeowners in 2022.

Retirement Savings Fall Short for Many

Now here’s where the anxiety kicks in. The median retirement savings for those aged 55-64 ($185,000) and 65-74 ($200,000) are far below that $1.26 million “magic number” Americans think they need to retire comfortably.

I know it sounds crazy, but the gap between expectations and reality is jarring. In 2024, 35% felt on track for retirement, up from 34% in 2023 but down from 40% in 2021, per a survey. The older the age group, the more likely they are to have retirement savings and feel as though their savings are on track.

Americans aged 65 to 74 saw a 54% increase to $409,900. While that might seem like a lot of money, this is the age bracket when many people retire and start tapping into their savings. The median tells a sobering story about what most people actually experience.

The Wealth Gap Keeps Growing

Wealth inequality didn’t just appear overnight. It’s been building for decades.

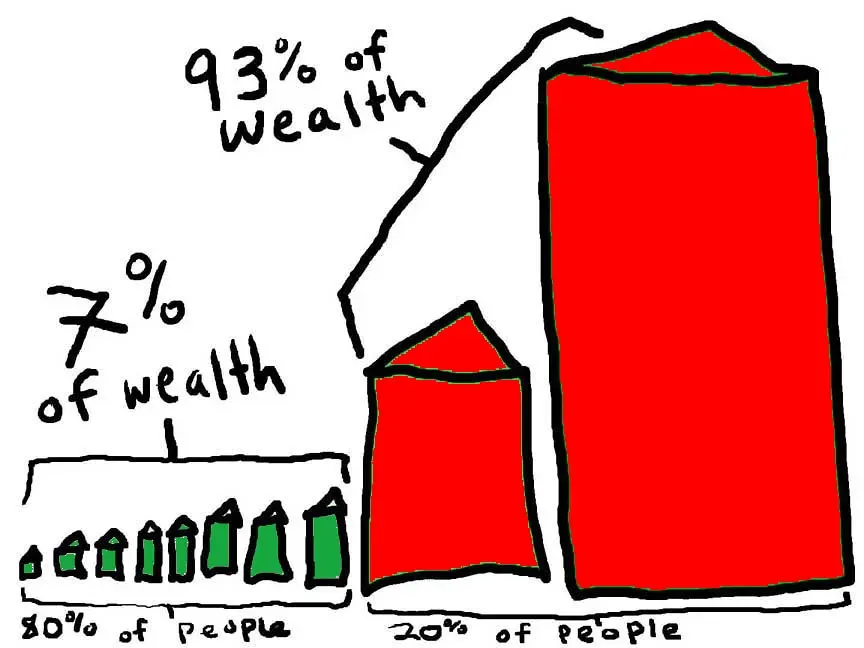

In 1989, the wealthiest families had 36 times the wealth of families in the middle of the wealth distribution. By 2022, they had 71 times the wealth of families in the middle. That shift happened during the lifetimes of today’s 71-year-olds, fundamentally changing what retirement looks like across income levels.

GAO’s analysis of HRS data also found that disparities in household income decreased while disparities in wealth persisted as a cohort of older Americans aged from approximately their 50s into their 70s or early 80s. Income disparities decreased between higher- and lower-earning households because higher-earning households saw larger drops in income over time, indicating the possible transition from working to retirement. For example, we estimated median income for the top mid-career earnings group decreased by 53 percent while estimated median income for the bottom earnings group decreased by 36 percent over the same period.

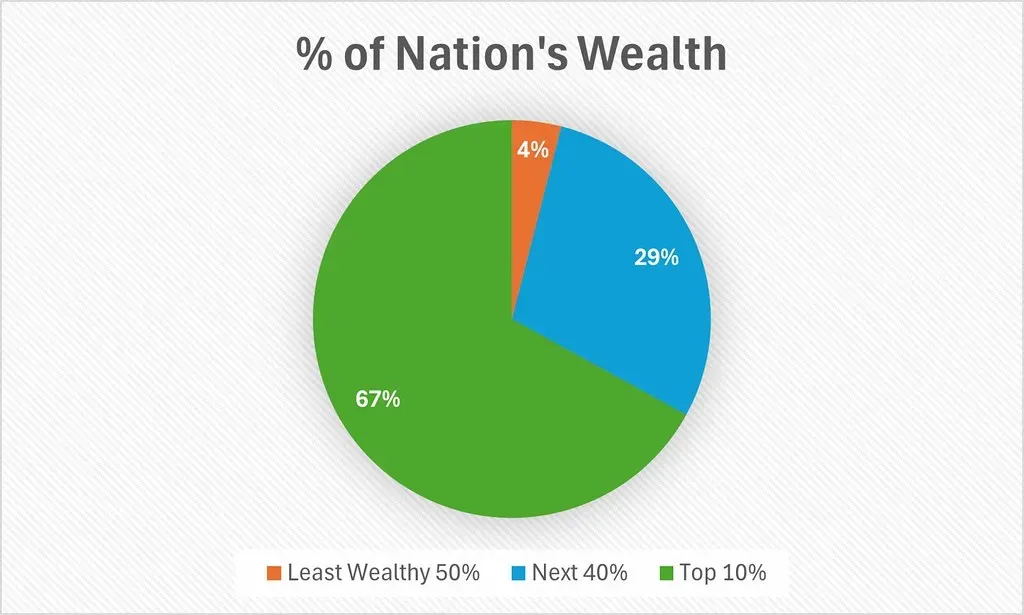

The wealth concentration at the top has only intensified. Wealth – the value of a household’s property and financial assets, minus the value of its debts – is much more highly concentrated than income. Federal Reserve data show that the least-wealthy 50 percent of U.S. households hold very little of the nation’s wealth (less than 4 percent), while the households with wealth in the top 10 percent hold over two-thirds. The concentration of wealth at the very top has increased over the past 35 years.

Where You Stand Depends on More Than Just Savings

Your position at 71 isn’t just about the dollars in your bank account. Net worth often peaks around retirement age, then declines as people begin withdrawing savings, spending down assets, and experiencing reduced income. Required minimum distributions, healthcare costs, and lifestyle spending all contribute.

A 2025 LendingTree report found that nearly all (97.1%) U.S. adults age 66 to 71 had non-mortgage debt, including auto loans, credit card bills and even student loans. Across the 50 largest metro areas, the median amount was more than $11,000. That debt burden eats into net worth figures and creates financial stress for people trying to stretch their retirement dollars.

Location matters enormously too. Housing markets vary wildly across the country, meaning identical savings might provide drastically different lifestyles depending on where you choose to live. Someone with $400,000 in net worth might live comfortably in one state but struggle in another where costs are higher.

So where do you stand? If you’re a 71-year-old American with a net worth around $400,000 to $450,000, you’re right in the middle. You’re not wealthy by any stretch, but you’re also not falling behind most of your peers. Honestly, that’s more reassuring than the inflated averages make it sound. Did you expect the gap between average and median to be that wide?