Medicare Part B Trap: The One Form You Must File at 65 to Avoid Lifetime Penalties

Turning 65 should feel like a milestone worth celebrating, not the beginning of a financial nightmare. Yet thousands of Americans stumble into a hidden Medicare trap every year that costs them hundreds, sometimes thousands, of extra dollars for the rest of their lives. The culprit? Missing a critical enrollment window and failing to understand when and how to sign up for Medicare Part B.

Here’s the thing that catches most people off guard. In 2016, only 60% of Medicare-eligible 65-year-olds were taking Social Security, compared to 92% in 2002, which means fewer people are being automatically enrolled in Medicare. If you’re not collecting Social Security benefits when you hit 65, you need to actively sign up yourself, and Medicare may not even notify you about your eligibility. Miss that window, and you could face penalties that never go away.

The Seven Month Window That Changes Everything

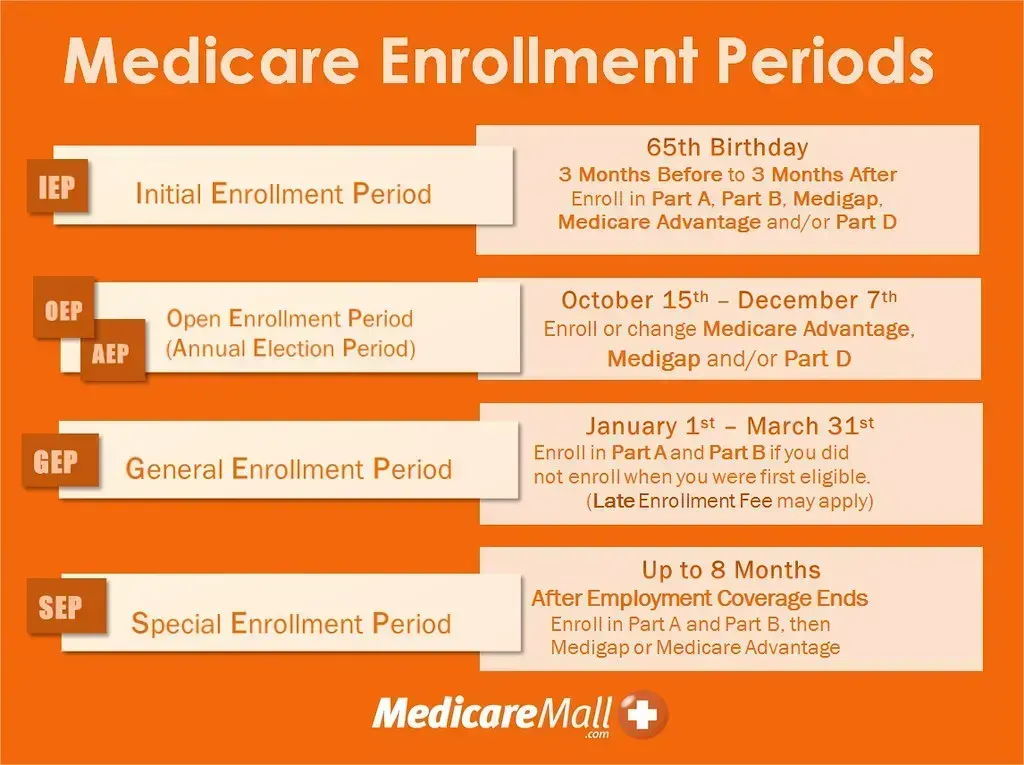

Your first chance to sign up for Medicare is called your Initial Enrollment Period. It lasts for 7 months. If you’re eligible for Medicare because of your age, the Initial Enrollment Period starts 3 months before you turn 65, and ends 3 months after the month you turn 65. Think of it like this: the government gives you a narrow runway to land your Medicare enrollment properly.

Let’s say your birthday falls in June. Your enrollment window opens in March and closes in September. Sign up during those months, and you’re golden. After completing your Initial Enrollment Period sign-up, your Medicare coverage start date depends on when you enroll: For example, if you complete your enrollment on June 25, your Medicare coverage will start on July 1. Miss that deadline without a valid excuse, though, and the penalties start piling up fast.

The Lifetime Penalty Nobody Warns You About

The late enrollment penalty adds an extra 10 percent of the standard Part B premium for each 12-month period when you could have had Part B but didn’t, and it lasts for as long as you have Part B. Let that sink in. This isn’t a one-time slap on the wrist.

Let’s say you delayed enrollment in Part B for seven years. Your monthly premium would be 70% higher for as long as you have Medicare (7 years x 10%). Since the base Part B premium in 2026 is $202.90, your monthly premium with the penalty will be $344.93. That’s an extra roughly 140 dollars every single month, for life. Over two decades of retirement, we’re talking about tens of thousands of dollars in unnecessary costs.

Who’s Getting Hit Hardest by These Penalties

The data reveals some troubling patterns about who ends up paying these penalties. In 2021, an estimated 779,400 Medicare beneficiaries were paying the Part B LEP, with the average penalty increasing their monthly premium by nearly 30%. That’s close to 800,000 Americans stuck with higher costs because they missed critical deadlines or didn’t understand the rules.

The share of Part LEP-payers was higher among American Indian/Alaska Native (2.5%), Hispanic/Latino (2.1%), Asian/Pacific Islander (1.8%) and Black (1.6%) enrollees than among White enrollees (1%). Geographic location matters too. In 2021, the portion of Part B enrollees paying a penalty ranged from 0.7% in Indiana to 3.1% in the District of Columbia. These disparities suggest that information about Medicare enrollment isn’t reaching everyone equally.

Perhaps most disturbing: One study estimates that about 20% of people paying the Part B LEP did not know about these penalties at the time they reached age 65. One in five people paying these penalties had no idea they existed when it mattered most.

The Employer Coverage Exception That Saves You

Now here’s where things get interesting, and frankly, a bit complicated. Not everyone needs to sign up at 65. If you or your spouse is still working and has healthcare coverage through an employer, you can wait to sign up for Part B without paying a penalty. But once your employer coverage is gone, the only way to avoid a penalty is to enroll in Part B during what’s called a Special Election Period. That’s an 8-month period that begins when your employer coverage ends or you stop working, whichever comes first.

The size of your employer matters enormously here. Medicare defines a “large employer” as any company that has 20 or more full-time employees. Work for a company with at least 20 people, and your insurance counts as creditable coverage, allowing you to delay Part B enrollment safely. Work for a smaller company? You need to sign up at 65, period.

The Creditable Coverage Form You Absolutely Need

Employers and other entities that offer health insurance to Medicare-eligible individuals are required to notify their policyholders about creditable coverage. They must provide a notice to their Medicare-eligible policyholders each year, usually by October 15, to inform them whether their prescription drug coverage is creditable or not. This is the document you cannot afford to lose.

Once you become eligible for Medicare Part D, your current insurer is required to let you know if your insurance provides creditable coverage for prescription drugs. If your current insurance is creditable, you’ll receive a creditable coverage disclosure notice. Keep this letter. You’ll need to show it to Medicare when you enroll to avoid having to pay late enrollment penalties.

Seriously, file this notice somewhere safe. Tape it to your refrigerator if you have to. When you eventually enroll in Medicare after leaving your job, this letter proves you had qualifying coverage and protects you from penalties. Without it, you might struggle to convince Medicare you deserve an exception.

What Doesn’t Count As Protection

This is where a lot of people get burned. COBRA (Continuation of Health Coverage) is designed to prolong your health insurance coverage if you’re no longer employed. It isn’t creditable coverage for Original Medicare but may be creditable coverage for Part D. If you decide to take COBRA, you must enroll in Medicare when you become eligible to avoid penalties. Read that again. COBRA doesn’t protect you from Part B penalties.

Retiree coverage, including COBRA, does not count as creditable coverage for Medicare. So if you retire at 63 with a nice retiree health plan from your former employer and think you’re all set until 65, you’re in for an unpleasant surprise. You still need to enroll in Medicare Part B during your Initial Enrollment Period at 65 to avoid penalties.

How to Enroll and What Forms to File

If you’re already receiving Social Security benefits at least four months before turning 65, congratulations, you get the easy path. You may be automatically enrolled in Medicare. You’ll receive your Medicare card in the mail before your 65th birthday. The government does the paperwork for you.

If you are not currently receiving Social Security or Railroad Retirement Board benefits when you turn 65, you’ll have to sign up for Medicare yourself. Medicare may not notify you about your eligibility, so be sure to get your Initial Enrollment Period (IEP) dates and put them in your calendar. You can enroll online at the Social Security Administration website, by calling 1-800-772-1213, or by visiting your local Social Security office in person.

The main form you’ll need is the Application for Enrollment in Medicare Part B. Take your time with it. Double check dates. Make copies for your records.

When You Can Fix Mistakes and Get Penalties Waived

Let’s say you already missed your window and you’re facing penalties. Is there any hope? Possibly. If you find yourself without Part B coverage or are paying a penalty because you received bad advice from the federal government, Social Security may be able to waive your Part B penalty, enroll you into Part B, or do both things.

This waiver aims to alleviate the financial burden on individuals who missed their Initial Enrollment Period (IEP) or Special Enrollment Period (SEP) due to valid reasons. Eligibility for the waiver typically depends on demonstrating that the delay in enrollment was due to circumstances beyond the individual’s control. Examples include receiving misinformation from a government representative, natural disasters that prevented enrollment, or being incarcerated.

The waiver isn’t automatic. You need to file an appeal and provide documentation supporting your case. It helps to involve your elected representatives who can advocate on your behalf with Social Security.

The General Enrollment Period Fallback Option

Miss your Initial Enrollment Period and don’t qualify for a Special Enrollment Period? You’re not completely out of luck, just temporarily stuck. You can sign up between January 1-March 31 each year. This is called the General Enrollment Period. Your coverage starts the month after you sign up. You might pay a monthly late enrollment penalty, if you don’t qualify for a Special Enrollment Period.

This is the “General Enrollment Period,” and there is typically a life-long penalty if you sign up during this time. So yes, you can eventually get coverage, but you’ll pay extra every month for missing your initial window. The General Enrollment Period is essentially your safety net with strings attached.

Action Steps Before You Turn 65

Start planning at least six months before your 65th birthday. Contact your human resources department or insurance provider to determine if your coverage qualifies as creditable. Request written confirmation. Employer/Union and other group health plans are required to provide Medicare-eligible employees with a Notice of Creditable Coverage each year by October 15th. Get that notice and keep it safe.

If you’re still working with a large employer, decide whether you want to delay Part B or sign up anyway. Some people enroll in both to lower out-of-pocket costs, even though Medicare becomes secondary insurance while you’re employed. If you decide to delay, mark your calendar for eight months after you retire or lose coverage. That’s your deadline.

Not working or with a small employer? Circle those three months before your 65th birthday on your calendar in red ink. Set phone reminders. Tell your spouse or adult children to nag you about it. Do whatever it takes to remember to enroll during your Initial Enrollment Period. The consequences of forgetting are too expensive to risk.

Understanding Medicare enrollment rules takes effort, but protecting yourself from lifetime penalties is worth the homework. Roughly 800,000 Americans are currently paying penalties that eat into their fixed retirement income every single month. Don’t let yourself become part of that statistic. Know your deadlines, understand your coverage, and file your enrollment paperwork on time. Your future self will thank you for paying attention now rather than paying penalties later.