The “Paper Millionaire” Risk: Why a $3M Net Worth May Not Feel Secure by 2030

Here is a number that should make you pause: Americans say they would need $5.3 million in net worth to feel financially successful, according to Empower research. So if you are sitting on what looks like a solid $3 million, you might be surprised to find out just how fragile that number really is. The gap between wealth on paper and wealth you can actually feel, spend, and rely on is wider than most people realize – and it’s growing every year.

America may be entering the era of the illiquid millionaire, a shift that is redefining what it means to be rich, with profound implications for both society and public policy. Millions of households carry seven-figure net worths that exist mostly in unrealized home equity, locked-up retirement accounts, or volatile stock portfolios. The number looks beautiful on a spreadsheet. Reality, as always, is far more complicated. Let’s dive in.

The Illusion of Millionaire Status in 2026

Let’s be real – the millionaire label has become almost ordinary. With approximately 24 million millionaires calling the United States home, nearly one in every twelve American adults has achieved this financial milestone. That sounds impressive until you consider what $1 million or even $3 million actually buys you today versus what it bought thirty years ago.

Back in 1990, the median home price was only $117,000. Today, the median home price is closer to $430,000. Think about that for a second. The price of an average American home has nearly quadrupled. If your “millionaire” status is being propped up by a single illiquid asset that tracks housing prices, you are in a very precarious position.

Using historical inflation data, $1 million in 1990 has the purchasing power of approximately $2.3 to $2.5 million in 2025. This means $3 million today is only modestly more powerful than $1 million was 35 years ago. The millionaire label simply hasn’t kept pace with the real world. It is, at best, a polished illusion.

What “Paper Wealth” Really Means – and Why It’s Dangerous

A paper millionaire is an individual whose net worth is largely based on the market value of their assets, such as securities, stocks, or other investments. The critical word there is “market value” – because markets move, and they don’t always move in your favor. Paper wealth is powerful when markets are rising. It evaporates shockingly fast when they fall.

This wealth is typically not secure until holdings are sold and profits are locked in. Without liquidation, a decline in the market might wipe out the gains entirely. The dot-com crash taught an entire generation this lesson. Many paper billionaires had invested in internet businesses during the dot-com bubble in the 1990s when valuations surged. Many gained millions of dollars – but were still classified as paper millionaires if they did not sell their shares for cash.

Honestly, the same risk is playing out today in different clothing. Rising home equity, inflated stock portfolios, unlisted private equity stakes – all of it looks great on paper. The moment you actually try to access that money, reality sets in.

The Liquidity Problem: Rich on Paper, Broke in Practice

Despite relative affluence, today’s millionaires rarely have anywhere near $1 million to spend however they want. For barely-millionaires – households with a net worth between $1 million and $2 million – the vast majority of that wealth is illiquid. They typically had roughly two-thirds of their wealth tied up in a primary home and retirement accounts in 2023, an increase of eight percentage points since 2017.

The difference between a poor millionaire and a rich millionaire is liquidity. The rich millionaire has easy access to their wealth. It sounds simple, but the consequences are enormous. A person with $3 million largely locked in their house and a 401(k) cannot easily pay for a medical emergency, a job loss, or a sudden market downturn without triggering penalties or fire sales.

A layoff, bear market, or job loss could quickly put illiquid millionaires in peril. In contrast, a rich millionaire – also worth over $1 million but able to easily tap into their wealth – is liquid and resilient to financial shocks. The distinction is not dramatic on a balance sheet. In real life, it is everything.

Inflation Has Quietly Hollowed Out the $3 Million Dream

Thanks to inflation, a millionaire today needs over $3 million to match the purchasing power of a 1990s millionaire. We keep moving the goalposts without acknowledging it. Think of $3 million like a long-distance runner who looks fast but is actually running into a fierce headwind the entire way. The number grows, but what it represents in real terms barely budges.

Inflation affects how much your savings can buy over time. When prices rise, the value of money goes down. Your $3 million may not stretch as far in 20 years as it does today. If inflation averages 3% a year, what costs $100 now will cost about $180 later. That’s not a minor inconvenience. That’s a structural threat to long-term financial security.

Rising costs in major categories – housing, childcare, healthcare, and college tuition – have outpaced general inflation for decades. Families in high-cost areas may spend $50,000 or more annually on just housing and childcare. When those costs compound year after year, even a $3 million cushion gets thin fast.

Healthcare: The Retirement Budget Destroyer Nobody Plans For

Here is the thing that shocks most affluent retirees: healthcare is not just expensive. It’s spectacularly, persistently, brutally expensive. The average 65-year-old who retired in 2025 expected about $172,500 on healthcare and medical expenses during retirement, not including potentially catastrophic long-term care costs, according to an annual survey by Fidelity.

A healthy 65-year-old woman could face $313,000 in total healthcare expenses over her retirement, compared with about $275,000 for a man, according to the 2025 Milliman Retiree Health Cost Index. And that’s if you stay reasonably healthy. Medical care prices have risen faster than overall consumer prices for more than two decades. From 2000 to June 2024, medical care prices increased by more than 121%, compared with roughly an 86% rise in all goods and services.

Healthcare costs consume roughly fourteen percent of withdrawals at age 65 – and nearly half by age 85, crowding out lifestyle spending even as your withdrawal rises with inflation. A $3 million portfolio starts to look a lot smaller once you run those projections honestly. Long-term care, including nursing homes, assisted living, and extended in-home support, is often the single largest uncovered expense in retirement. Nearly 70% of retirees will require some form of long-term assistance, but Medicare covers very little of the cost.

Sequence of Returns Risk: The Timing Problem That Can Break You

Most people understand market risk in the abstract. They accept that markets go up and down. What they often don’t appreciate is how devastating bad timing can be specifically during the early years of retirement. Sequence of returns risk means the order your investment returns come in matters more than the long-term average. A 20% market drop in Year 1 of retirement does far more damage than the same drop in Year 15 – because you’re selling shares at depressed prices to fund withdrawals, permanently reducing the portfolio’s recovery potential.

Sequence of returns risk highlights how market return timing impacts portfolio sustainability. Poor returns early in retirement, when withdrawals are a larger portfolio percentage, can severely diminish longevity. Imagine two retirees both starting with $3 million. One retires in a boom year; one retires when markets drop twenty percent. After a decade, their outcomes can diverge by hundreds of thousands of dollars – despite identical spending habits.

If markets fall 20%, you lose $600,000 in value and must reduce income or risk depletion. On a $3 million portfolio, that’s not a small correction. That is a potentially irreversible restructuring of your entire retirement plan. It’s hard to say for sure how markets will behave by 2030, but history suggests volatility is not going away.

Geography Changes Everything: Where You Live Determines If $3M Is Enough

Geography dramatically changes what $3 million “feels” like in practice. A portfolio that funds a luxurious retirement in one location may feel merely adequate in another. This is a detail that gets glossed over in general financial advice, but it matters enormously. $3 million in rural Tennessee and $3 million in San Francisco are not remotely the same financial reality.

In a high-cost city like Los Angeles, $120,000 after taxes may cover housing, health insurance, and basic lifestyle without much cushion. Sequence-of-returns risk is significant: a major bear market in the first five years could permanently impair the portfolio. Medical expenses before Medicare and California state income tax add pressure. That’s the reality for a single retiree with a $3 million nest egg in a major metro area.

State taxes are one of the most underestimated drags on portfolio longevity. Every dollar withdrawn for state taxes is a dollar that can’t compound – and at a 6% return, $10,000 withdrawn today represents approximately $57,000 in lost value over 30 years. Geography isn’t just about lifestyle. It is literally a financial variable that can determine whether your money lasts.

The Psychological Trap: Why Wealthy People Still Feel Broke

Many households with $3 million still experience genuine financial anxiety. The number sounds impressive, but real life often feels different. This isn’t weakness or ingratitude – it’s a structural disconnect between what the numbers say and what daily financial life actually feels like when most of that wealth is locked away or subject to constant threats.

In industries like tech, finance, and medicine, your peers may have $10 million, $20 million, or more. In wealthy neighborhoods, keeping up with much richer neighbors distorts your sense of where you stand. Social comparison is a brutal and underappreciated force in personal finance. When your baseline shifts to those around you, $3 million can genuinely feel inadequate – even if it objectively shouldn’t.

I think this psychological dimension gets dismissed too quickly by financial commentators who focus only on spreadsheet math. The emotional reality of wealth is real and it shapes financial decisions in meaningful ways. Feeling financially insecure can paradoxically lead to riskier investment behavior, underspending during retirement, or chronic anxiety that diminishes quality of life.

The Widening Wealth Gap and What It Means for the $3M Household

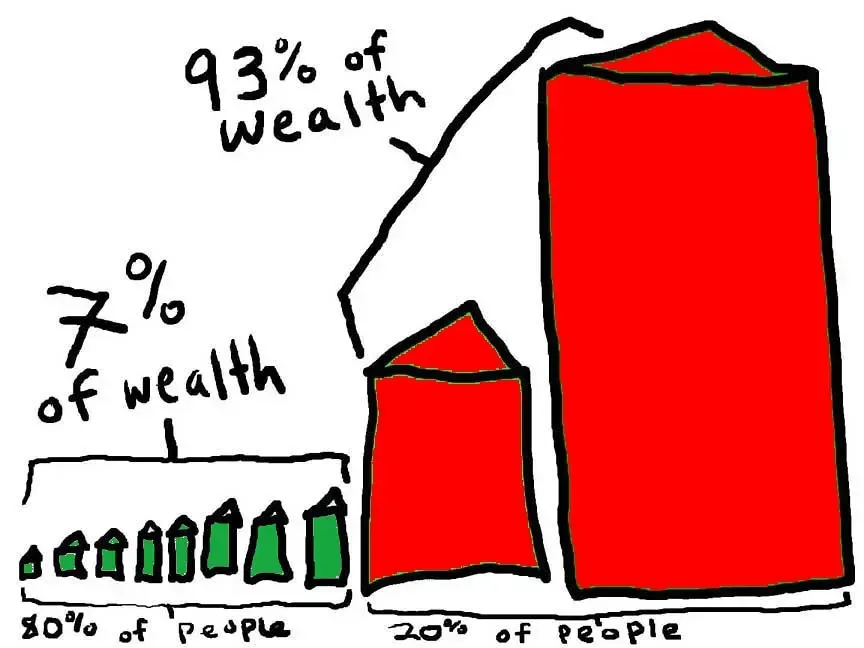

In 2025, wealth in the United States crossed an extraordinary threshold. The top 1% of Americans – those with a minimum net worth of $11.2 million – now command a record $52 trillion in combined assets, according to the Federal Reserve’s latest data. That context matters enormously. The $3 million household isn’t just measuring itself against an abstract benchmark. It exists in an economy where extreme wealth concentration affects everything from housing costs to tax policy to the cost of services.

Between April and June 2025, the top 1% amassed roughly 31% of all household wealth, nearly matching the combined assets of the bottom 90% of Americans. When wealth is this concentrated at the top, it drives up the costs of the very things that people with $3 million net worths rely on: real estate, healthcare, private school tuition, and luxury goods. Though the bottom 90% of Americans collectively hold $54 trillion in wealth, their relative share of national capital continues to erode. The majority of their assets are illiquid – tied to real estate, retirement funds, and small business ownership.

The $3 million household sits in a strange no man’s land – too wealthy to qualify for safety nets, too illiquid to truly feel secure, and increasingly squeezed by an economic system that rewards the very top far more than everyone else.

What Needs to Change: Rethinking the Path to Real Financial Security

To feel comfortable, aim to keep your primary residence below 30% of your net worth. To feel genuinely rich, keep it below 20%. That way, at least 80% of your net worth can be in liquid or semi-liquid assets. This single ratio can transform the feeling of wealth more than almost any other move. It is structural, not cosmetic.

Morningstar’s December 2025 research put the safe starting withdrawal rate at 3.9% for a 30-year retirement with 90% confidence. On $3 million, that’s $117,000 per year before taxes. That’s a comfortable income – but not an extravagant one, especially once taxes, healthcare, housing costs, and inflation take their bites. Additional income sources, such as rental income or annuities, can support a desired lifestyle and provide steady payments every month. Diversification of income streams, not just assets, is the real key to resilience.

Disciplined financial habits, consistent investing, and long-term planning remain the primary drivers of millionaire status in 2026. Yet long-term planning increasingly requires rethinking what the target should actually be. The number that once meant freedom may now just be the starting line. A staggering $83.5 trillion in wealth is set to be passed on to younger generations by 2048 through the great wealth transfer – which means the entire architecture of what wealth means and who holds it is about to shift dramatically before 2030 even arrives.

A $3 million net worth is genuinely impressive by most historical standards. But in 2026, with structural inflation, soaring healthcare costs, illiquid assets, widening inequality, and rising longevity, “impressive” and “secure” are no longer the same thing. The paper millionaire sits on a number that looks strong in every direction – until the moment it has to actually do something. What would you do if you woke up tomorrow and realized your $3 million couldn’t actually be spent? Tell us in the comments.