10 Things You’ll Always Notice in Homes of People Who Retired the “Old-School” Way – A Stark Contrast to Today

There is something quietly fascinating about stepping into the home of someone who built their retirement the hard way – or, more accurately, the patient, disciplined, decidedly analog way. No robo-advisors. No crypto wallets. No app telling them whether to rebalance their portfolio. Just decades of steady work, a monthly pension check, and a stubbornly full filing cabinet. The contrast with how today’s retirement landscape looks couldn’t be more dramatic if it tried.

More than 4 million Americans were reaching age 65 each year from 2024 until 2027, and they’re not all arriving with the same financial foundation. Some carry the unmistakable fingerprints of a retirement style that simply doesn’t exist anymore. Walk into their homes, and you’ll see the evidence everywhere. Here’s what to look for – and the surprising story behind each one.

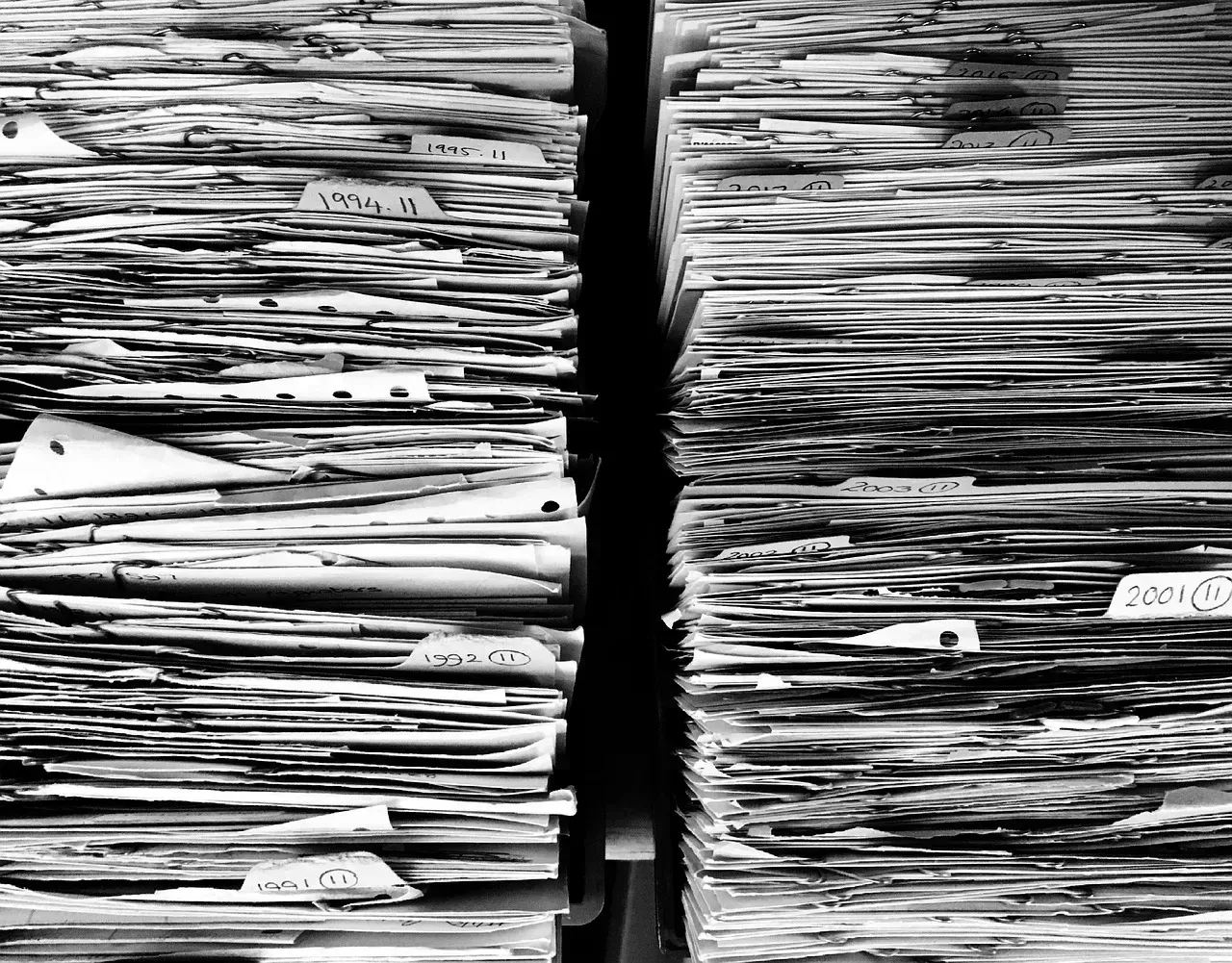

1. A Physical Filing Cabinet Stuffed with Pension Paperwork

Walk into the study or spare bedroom of a classic old-school retiree and you will almost certainly find it: the cabinet. Not a sleek cloud storage account, not a password-protected digital vault – an actual metal cabinet, probably slightly dented, with labeled folders going back decades. Tax returns from 1987. Union agreements. Defined benefit pension statements. It’s a paper archive of a life’s work.

This is no accident. The Boomer generation was the last to have widespread access to workplace pensions, and with expected retirement income from pensions, many didn’t feel the need to save as much as succeeding generations. That pension was the whole plan – and a pension generates a lot of paperwork.

Nearly a quarter of the Peak 65 Boomer group has a defined benefit pension, and around half of those pensions come from private employers while the other roughly half comes from state and local governments or the military. Today’s younger retirees, by contrast, are far more likely to manage everything through a phone app. The physical cabinet is, honestly, a relic of a more tangible era of trust.

2. A Landline Phone – Still Plugged In

It’s not nostalgic. It’s not ironic. It’s just there, sitting on a side table or mounted to a kitchen wall, fully operational. For people who retired the old-school way, the landline is a symbol of stability – and that value runs deeper than any telephone line. These are people who built their lives on things that didn’t change every two years or require a software update.

There’s a broader habit here worth noticing. Cash is an essential aspect in Baby Boomers’ financial toolbox, with more than two in five (42%) saying they carry cash with them every day, and cash making up a substantial portion of their average asset allocation. The landline fits the same psychological pattern – keep what works, trust what you can touch, and don’t replace something just because something newer exists.

Younger generations streaming calls through wifi-dependent smartphones would find this baffling. To old-school retirees, it’s just sensible. The landline always works during a power outage, never runs out of battery, and never asks you to agree to new terms and conditions. That’s a kind of freedom, honestly.

3. Framed Social Security and Pension Benefit Statements on a Bulletin Board

You’ll often notice a small bulletin board, a refrigerator door, or a dedicated wall space near the kitchen desk where key financial figures are pinned up – visible, tangible, and regularly consulted. Monthly Social Security benefit amounts. Annual pension income. A handwritten budget. It’s a control room for fixed income, and it says everything about how this generation managed money.

The average expected Social Security benefit for peak boomers is about $22,000 a year. For old-school retirees who also carry a pension, that number is supplemented considerably. According to 2022 data from the Pension Rights Center, the median annual benefit for government pensions was about $25,980, while the median military pension was $24,130 – more than twice the median annual benefit of private pensions, which was just $11,040.

Knowing exactly what comes in each month, to the dollar, is a cornerstone of this retirement style. The bulletin board isn’t clutter – it’s the dashboard. Today’s retirees are more likely to glance at an app dashboard. There is something grounding about seeing the numbers pinned to a real wall, where they can’t disappear with a dead battery.

4. A Paid-Off Home with Zero Mortgage Anxiety

Here’s the thing about old-school retirees: many of them own their homes outright. No monthly mortgage draining a fixed income. No refinancing nightmares. Just a quiet, settled ownership that younger generations currently stare at from an astronomical distance. This isn’t luck, though timing certainly helped.

About three-quarters of boomers say their generation got lucky buying homes when they did. According to Federal Reserve data, Baby Boomers hold roughly half of the nation’s home equity, amounting to $17.3 trillion as of the second quarter of 2024. That equity is sitting in millions of paid-off homes – quiet, valuable, and deeply stabilizing.

Over half of boomers are mortgage-free and enjoy significantly lower housing costs, with median monthly expenses sitting around $612 for those without mortgages, covering taxes and insurance. About half of boomer homeowners say their current home fits their lifestyle needs or they prefer to age in place, and the low housing expenses that come with a fully paid-off mortgage are keeping roughly two in five boomer homeowners in place. Compare that to today’s retirees wrestling with high-interest rates and you start to understand why the house itself is one of the most defining symbols of old-school retirement.

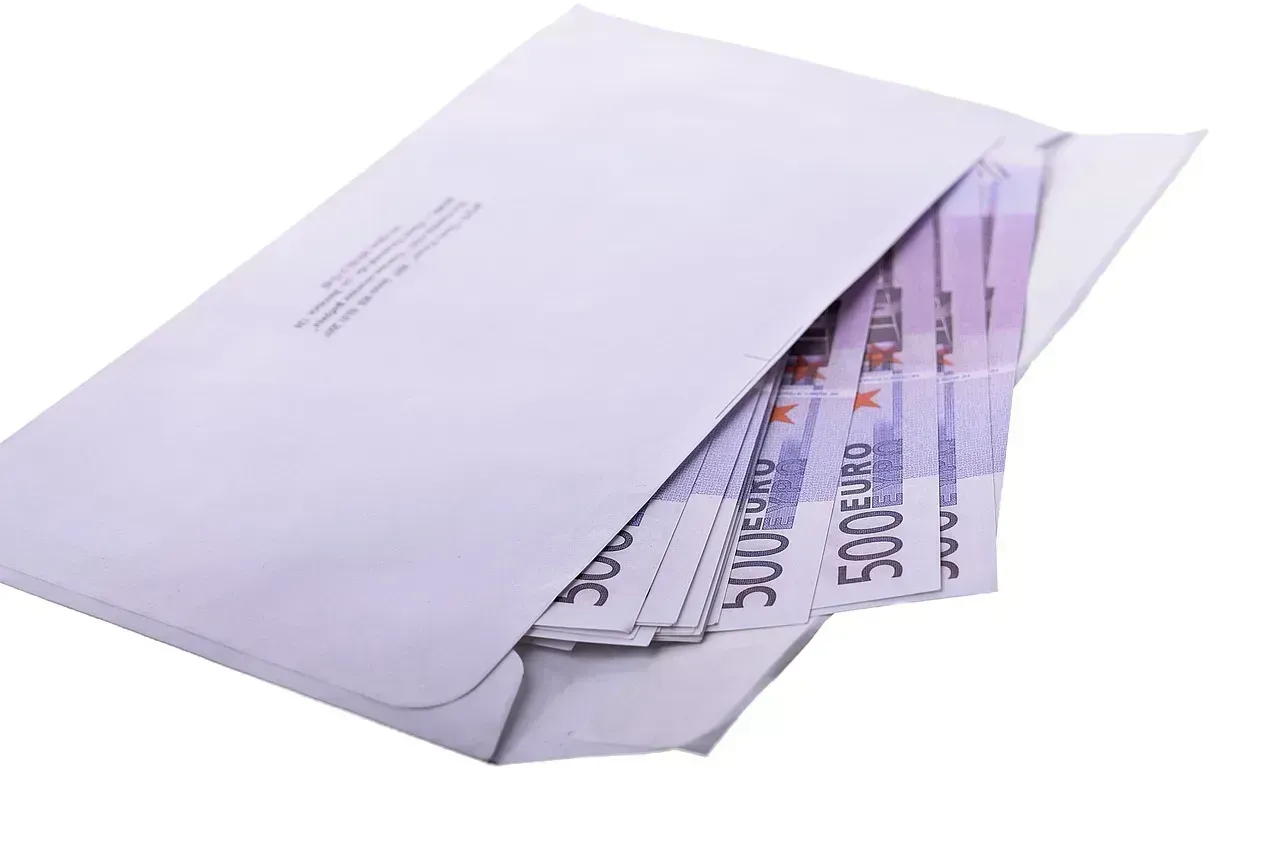

5. A Separate “Emergency Cash” Drawer or Envelope

Open the right kitchen drawer in an old-school retiree’s home and there’s a decent chance you’ll find an envelope with a small stack of bills. Maybe a hundred dollars. Maybe several hundred. Not a fortune, but a deliberate, physical emergency fund. This isn’t carelessness – it is a deeply ingrained financial habit formed decades before contactless payments existed.

Baby Boomers have a median emergency savings of $1,000, which is the highest amount across all generations. That figure makes sense when you consider that this generation lived through the stagflation of the 1970s, recession cycles, and the era before ATMs were on every corner. Cash on hand wasn’t paranoia – it was preparation.

Today, a Millennial might keep their emergency fund in a high-yield savings account, accessible via an app in seconds. The old-school retiree keeps theirs somewhere they can hold it. There’s a philosophical gap there that goes well beyond personal finance. It’s about trust. And about what “secure” actually means to different generations.

6. A Wall Calendar Marked with Fixed Income Deposit Dates

Not a digital calendar. Not a reminder on a phone. A paper wall calendar, hung in the kitchen or near the desk, with certain dates circled in red pen or highlighted in yellow. Pension deposit day. Social Security check date. The quarterly dividend from that utility stock they’ve held since 1994. It’s a financial rhythm made visible.

About nine out of ten Boomers receive Social Security benefits, and the average monthly Social Security benefit for a retired worker was $1,907 as of 2024. For those who also draw from a pension, fixed income arrives like clockwork on predictable dates. Planning life around that rhythm is second nature to this generation – and the wall calendar is how that rhythm gets anchored to the physical world.

Social Security is designed to replace only about 40% of a person’s annual pre-retirement income, on average. That gap between Social Security and full living costs is exactly why old-school retirees are so meticulous about marking every income date. Missing or forgetting a deposit date isn’t just inconvenient – it can throw off an entire month’s carefully managed budget.

7. A Dedicated “Bills Paid” Binder with Physical Receipts

Somewhere near the home office area – or even on a kitchen counter – old-school retirees often maintain a binder. Inside: utility receipts, insurance payment confirmations, property tax receipts, and phone bills going back years. Some of these binders have tabs. Color-coded tabs. This is not disorganization. This is an extremely organized, extremely analog record-keeping system that has worked without interruption for forty years.

Planning appears to be strongly linked to financial literacy and is an important determinant of household net worth at retirement, according to research from the National Bureau of Economic Research. The physical binder is a manifestation of that planning mindset. Everything documented. Everything cross-referenced. Nothing delegated to a server you can’t physically access.

Today’s retirees get PDF statements emailed to an inbox they may or may not check regularly. There’s an argument – a legitimate one – that the paper binder is more reliable. Hard drives crash. Email accounts get hacked. A binder on a shelf doesn’t require a password reset. Let’s be real: the analog approach has its very genuine advantages.

8. A Modest But Long-Held Investment Portfolio Printed on Paper

Old-school retirees who built wealth in the markets often have their portfolio printed out. Literally printed, on paper, from a broker statement or a monthly account summary. These aren’t day traders checking live tickers on a phone. These are people who bought blue-chip stocks, utility companies, and maybe a bond or two, and then mostly left them alone for twenty years.

Baby Boomers appear to be focused on keeping their wealth safe, with their investor holdings tilting toward less volatility. Fixed-income investments seem top of mind for this group more than any other generation, with more than one in ten of their asset allocation made up of U.S. bonds, compared to Gen X who hold about half that proportion.

As Allianz researchers pointed out, Baby Boomers benefitted from “a unique historical situation – strong economic growth, affordable housing markets, and booming equity markets” which coincided for a large portion of their adult lives, enabling them to build up sizable retirement nest eggs. The printed portfolio statement on the desk is a monument to patient, slow-and-steady investing – a style that is increasingly rare and arguably increasingly undervalued.

9. Long-Term Care Insurance Documents in Plain Sight

Old-school retirees who planned thoroughly often have one more thing you won’t see in most younger households: long-term care insurance paperwork. Usually stored somewhere accessible – top of the filing cabinet, a labeled folder on the shelf – alongside healthcare documents, Medicare cards, and supplemental coverage details. This generation understood something viscerally: medical costs in retirement are serious.

The average Boomer couple retiring at 65 needs about $315,000 for medical expenses over the course of retirement. That is a number that stops most people cold when they first see it. In fact, about seven in ten adults who live to age 65 will experience a long-term care event during their lifetime. Old-school retirees who planned ahead knew this, and the documents in their homes reflect that foresight.

One critical retirement mistake that boomers often make is underestimating healthcare costs. Many retirees don’t fully account for the expenses associated with medical care, long-term care, and prescription medications, which can significantly impact their savings and financial security during retirement years. The ones who got it right? Their paperwork tells the story. Prominently filed. Carefully organized. Ready to be found when needed.

10. A Deep Sense of Financial Quiet – No Debt Conversation Happening in the House

This last one isn’t a physical object. It’s an atmosphere. Step into the home of a retiree who built their financial life the old-school way, and there’s a particular calm about money. Not wealthy calm, necessarily. Just settled. No looming credit card balances being discussed at the dinner table. No refinancing stress. No anxious budget app refreshing on a phone screen. The house breathes differently.

Boomers typically have fewer debt obligations that constrain spending, in contrast with younger consumers who carry higher average debt profiles including mortgages, student loans, and car loans. For the truly old-school retiree, that freedom from debt isn’t accidental – it’s the result of decades of living within their means, something that sounds simple and is, in practice, incredibly hard.

Among the reasons for some boomers’ more precarious financial position relative to older generations: the workplace retirement system shifted from a pension-heavy system to a 401(k)-type system right as younger boomers were in their peak earning years. Those who escaped that shift – who retired with a solid pension and a paid-off house – live in a financial environment that today’s retirees are largely struggling to replicate. The quiet in that house is earned. And increasingly rare.