I Moved to Florida to Retire and Regretted It – 5 Reasons I Eventually Left

Florida has long held a near-mythical status in the American retirement imagination. Warm winters, no state income tax, and miles of coastline – it seemed like the perfect reward after decades of hard work. I believed all of it. I packed up, sold my house up north, and headed south with high hopes and a retirement budget I thought was solid. Within a few years, I was packing again – this time, heading out. Here is exactly why.

1. The Cost of Living Blindsided Me

Once considered the ideal place to live out one’s golden years, Florida is quickly losing favor with retirement-aged folks. Remote workers and the wealthy are flocking to the state and driving up home prices, leaving those on a fixed income feeling the pinch. When I moved, I thought the no-income-tax perk would stretch my retirement savings significantly. What I didn’t fully account for was how dramatically and quickly every other expense would climb. In just half a decade, the median price of a single-family house in Florida rose $150,000, or roughly 60%. According to Redfin, the average cost of a home in March 2018 was approximately $250,000. By July 2024, the median sale price had climbed to $409,700.

Even if you already own your home, rising costs for maintenance, HOA fees, and utilities can slowly chip away at your fixed income. Groceries and gas are more expensive than in many other states, and once you factor in sales taxes, property taxes, and hidden fees, the overall affordability starts to fade. There’s also the matter of grocery costs. Grocery prices in Florida experienced a notable increase, with a 4.3% rise between March 2024 and March 2025. Retirement savings that once looked comfortable started feeling very thin, very fast. For decades, the “Florida plan” was simple: you endured the northern winters, saved your money, and in exchange, you got to retire to a subtropical tax haven. But if you look at the math in 2026, that deal is dead. Florida has gentrified into a luxury product.

2. The Home Insurance Crisis Was a Gut Punch

Nobody warned me clearly enough about this one. Florida’s homeowners insurance market has been in a state of prolonged crisis, and retirees on fixed incomes have absorbed the worst of it. Roughly 70% of Florida homeowners have experienced rising insurance costs or coverage changes – such as their insurer dropping them – a 2024 Redfin survey found. Insurify’s home insurance price projections expected Florida’s premiums to rise another 9% in 2025, reaching an average of $15,460 annually – that’s $1,320 more than in 2024.

Florida was hit by the two most destructive disasters of 2024, according to Munich RE. Hurricane Helene, which made landfall in September, caused $56 billion in overall losses and $16 billion in insured losses. Hurricane Milton, which hit the state two weeks later, caused $38 billion in overall losses and $25 billion in insured losses. The scale of those storms sent shockwaves through the insurance industry. Florida homeowners pay about 148% more than the national average, making it the most expensive state for property insurance. Retirees who move to Florida are often shocked to discover that deductibles for hurricane insurance often range from 2% to 5%, and sometimes as much as 10%, of the policy coverage – rather than the fixed dollar amount they were accustomed to up north.

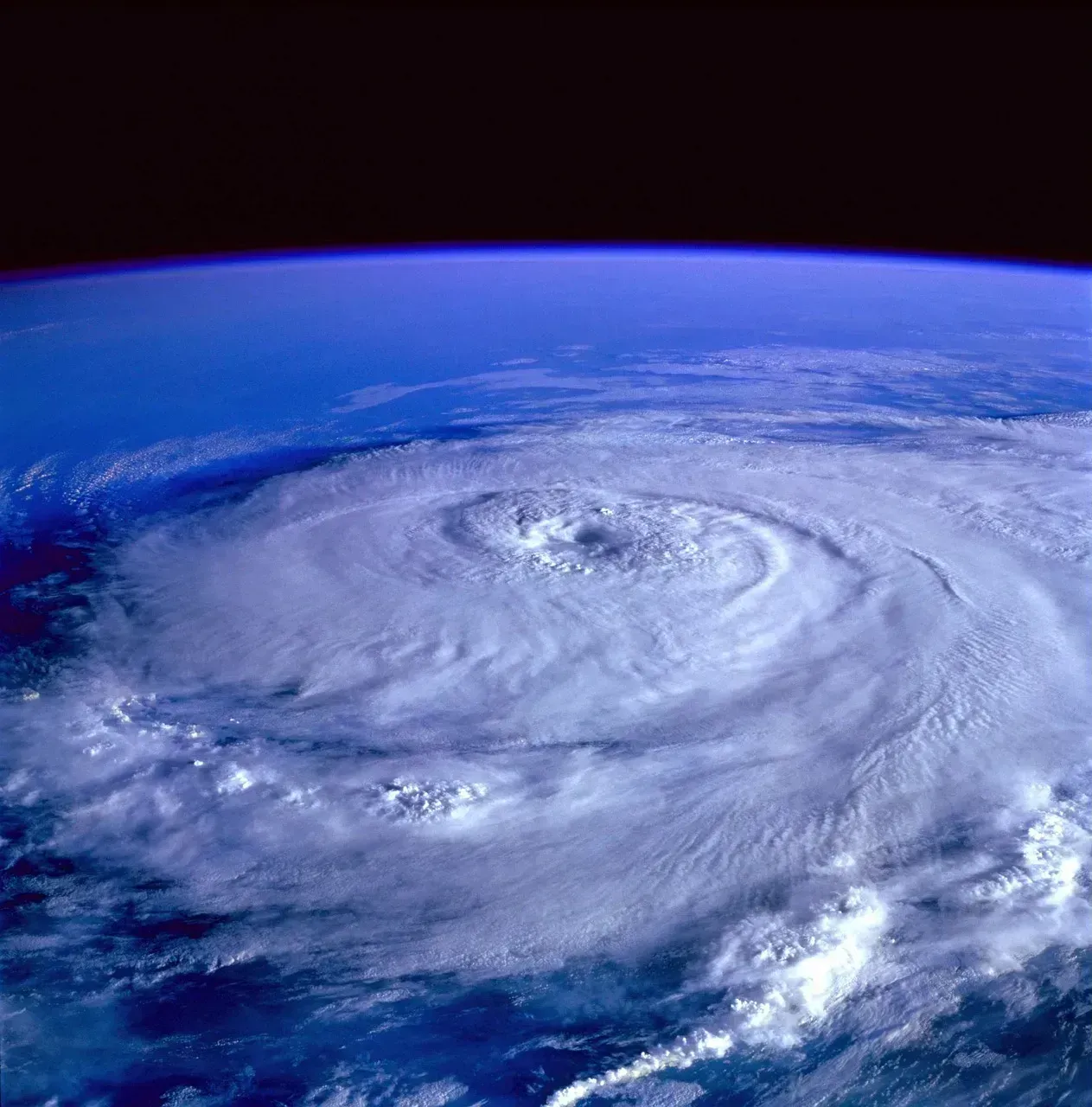

3. Hurricane Season Wore Me Down Mentally

The physical danger of hurricanes gets all the headlines, but the psychological cost is something nobody mentions in retirement brochures. There’s the stress brought on by hurricanes. Most Floridians have to keep a go-bag ready for last-minute evacuations and be prepared to leave behind what they can’t fit in their car. Just the stress of anticipating hurricane season can be enough to send people packing. I lived June to November in a state of low-grade anxiety every single year. That is not how retirement is supposed to feel. The National Centers for Environmental Information report that the state was hit with 94 disaster events between 1980 and 2024. In September 2024, Hurricane Helene hammered Florida and the Southeast, killing more than 230 people, making it the deadliest hurricane to strike the U.S. since Hurricane Maria in 2017. Some estimates put the economic impact as high as $200 billion, which makes this storm the costliest in U.S. history.

The 2024 hurricane season led many retirees in the Southeast to reconsider their proximity to the coast and seek more stable climates where their Social Security checks can stretch further. I was one of them. What is new is how frequent and powerful hurricanes have become. In recent years, Florida has seen several devastating storms, and the pattern is starting to worry long-time residents. Power outages, evacuations, damaged homes, and flooded streets are no longer rare events. They’re becoming part of the regular conversation. After one too many sleepless nights tracking storm paths on my phone, I made up my mind.

4. The Overcrowding and Infrastructure Pressure Were Relentless

Florida’s population growth sounds like a positive on paper, but living inside it is a very different experience. Florida is the third most populous state, with between 300,000 and 380,000 new residents arriving each year. Its aging infrastructure is scrambling to keep up, and it’s a seller’s market as developers try to meet demand. Overburdened health services have driven away many retirees who depend on regular care. As the third most populous state, Florida’s population reached 23 million in 2024 and is projected to exceed 24 million by 2027, driving significant pressure on the state’s transportation infrastructure.

Florida’s public transportation system has long been ranked as one of the worst in the country. Despite spending more on highways than many neighboring states, Florida has one of the worst highway systems in the nation, with high fatalities and commute times compared to other states. Simple errands that should take 15 minutes were taking an hour. Hurricane risks, tourists causing crowding and traffic congestion, very high homeowners insurance premiums, and rising HOA fees in most areas are now widely cited drawbacks for Florida retirees. The peace and quiet I had imagined for my golden years simply did not exist in the version of Florida I landed in.

5. The Healthcare Reality Did Not Match the Promise

This was the factor that truly sealed my decision to leave. I had assumed that a state full of retirees would have a world-class healthcare system designed to serve them. The reality was far more troubling. A 2025 WalletHub study ranked Florida at number 42 in the entire country – firmly among the bottom ten worst healthcare systems nationwide. That ranking alone should give any retiree planning a Florida move serious pause. Long-term care in Florida, which Medicare tends not to cover, can reach anywhere from $63,000 to over $130,000 per year, depending on how much attention is required, according to 2024 data from Genworth. For a retiree on a fixed income, those numbers aren’t just alarming – they’re potentially ruinous.

There are multiple reasons some retirees are less drawn to Florida these days. Once a strong point, the state’s cost of living is on the rise as an increasing number of remote workers settle there. Climate change and the dangers of natural disasters are a factor, as are related spikes in insurance costs. Concerns around healthcare are also increasing. Florida, unfortunately, is on the higher end of the savings-requirement spectrum. The annual cost of living minus Social Security income leaves retirees needing a minimum of roughly $736,588 in savings to cover 20 years of retirement. For many middle-class retirees, that number is simply out of reach – and the healthcare system designed to catch them when things go wrong is not equipped to do so reliably. That reality, more than anything else, is what put me back on the road heading north.